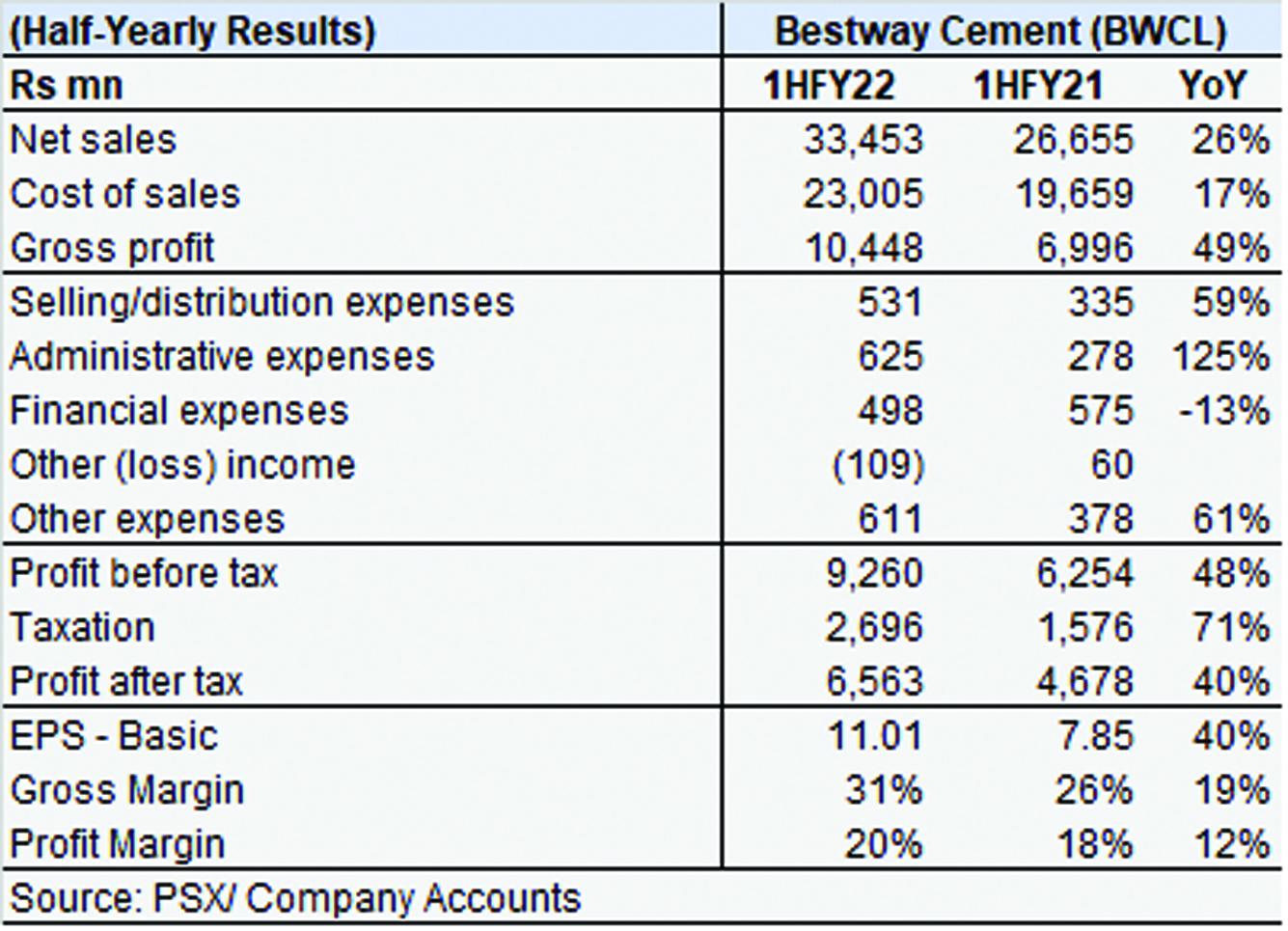

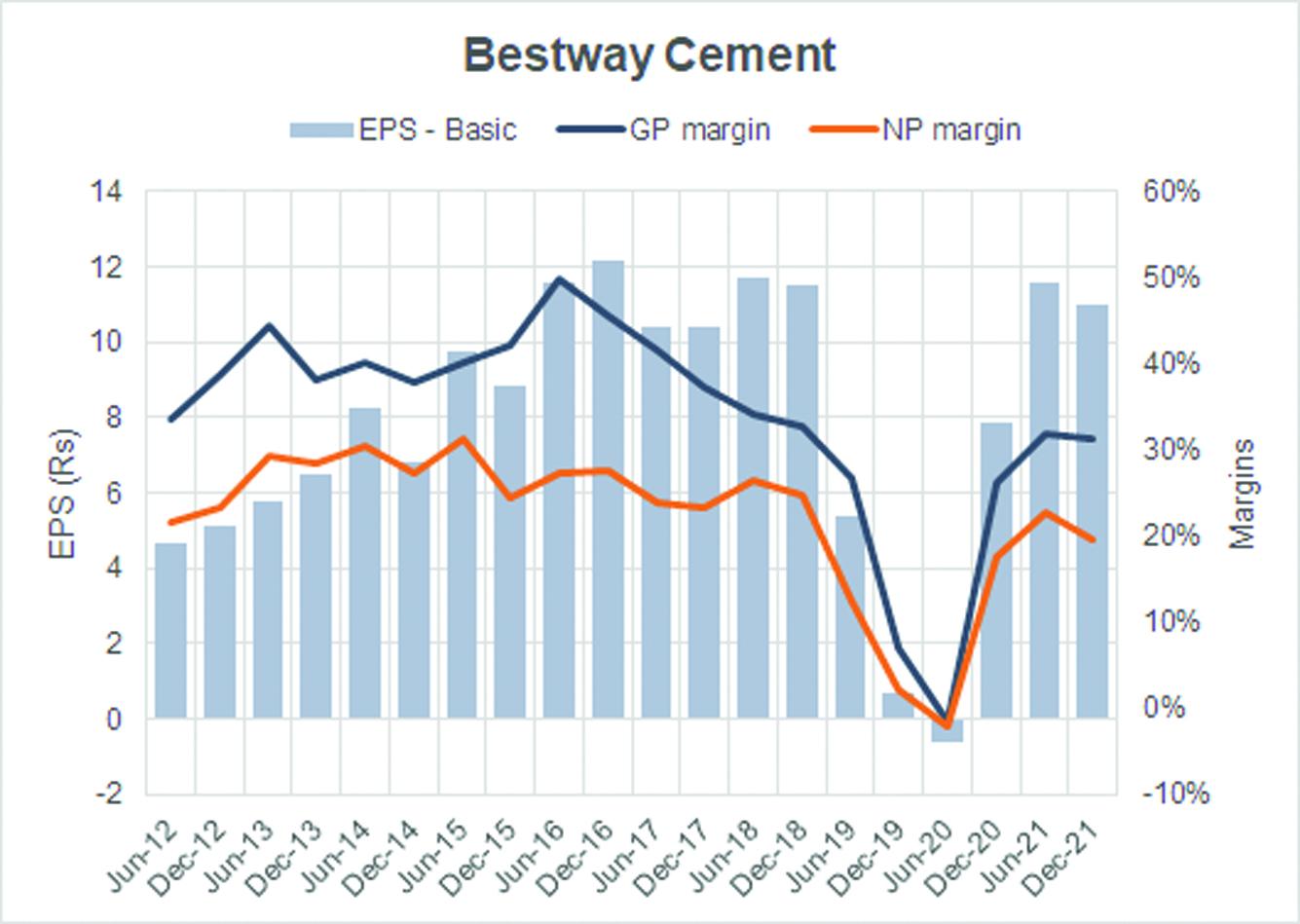

Despite getting knocked off from the lead by Lucky Cement some time ago (in terms of capacity), Bestway Cement (PSX: BWCL) stands out in its financial performance boosting the highest earnings in million rupees during 1HFY22 within the industry. The company’s margins also remain unrivalled during the period, not quite touching the peaks of FY16 but getting closer to FY18 and FY19, and substantially improved from last year. In an attempt to signal confidence, the company has also offered an interim cash dividend of Rs4 per share (40%) to shareholders.

This performance is credited to improved retention prices that cement manufacturers in the north have enjoyed this quarter, despite a visible slowdown in demand. Bestway’s offtake fell 8 percent with local dispatches declining 5 percent and exports plummeted to a near-halt by 67 percent owing primarily to the political uncertainty and ensuing worsening economic climate in Afghanistan. Bestway’s top-line however grew 26 percent in this scenario. Revenue per ton sold surged by 37 percent.

Against this backdrop are the rising cost of fuel, particularly coal which has wreaked havoc in global markets, and are once again on the rise amid the Russia-Ukraine war crisis. Cement manufacturers have been procuring coal from Afghanistan which was 10-15 percent cheaper than other sources abroad such as South Africa until a month ago but that too is following an upward trajectory. Thus far, cement manufacturers have mitigated their cost risks by bringing Afghan coal into the coal mix, but costs will rise rapidly in the upcoming quarters as cost scenarios develop. Bestway’s cost per ton sold grew 28 percent, lower than the revenue per ton sold for the company resulting in improved margins of 31 percent (1HFY21: 28%), the highest gross margins in the industry right now.

The company’s overheads and borrowing costs together constitute about 6 percent of revenue, same as last year, not too significant a dent on earnings.

With coal costs on the up and retention not expected to keep going up, amid export markets experiencing a slump, the burden of continued profitability falls on domestic demand. Even though warnings bells have been rung, Bestway is looking pretty good right now. More on demand later.

Comments

Comments are closed.