AGP Limited (PSX: AGP) was established as a public limited company in 2014 under the repealed Companies Ordinance, 1984 (now Companies Act, 2017). In 2018, it was listed on the country’s stock exchange. The company imports, markets, exports, and otherwise deals, distributes and manufactures all kinds of pharmaceutical products. It is a subsidiary of OBS Pakistan and the ultimate parent company is West End 16 Pte Limited- Singapore.

Shareholding pattern

As at December 31, 2021, over 71 percent shares are held under the associated companies, undertakings and related parties. Within this category, a major shareholder is Aitkenstuart Pakistan (Private) Limited. Over 15 percent shares are held under the category of “others”, while the local general public owns 5 percent of the shares in the company. The directors, CEO, their spouses and minor children own less than 1 percent shares while the remaining roughly 8 percent shares are with the rest of the shareholder categories.

Historical operational performance

The company has mostly seen a growing topline while the profit margin shave remained more or less stable over the years.

In CY18, revenue grew by nearly 14 percent to cross Rs 5 billion in value terms. This was primarily due to a substantial government institutional order for Hepatitis C products, in addition to a number of product launches. But this did not translate into higher profitability as gross margin reduced to 56.5 percent, compared to last year’s 60.8 percent. This was due to small margins on the government institutional order that made a large portion of the revenue. Moreover, currency devaluation also drove profits down. Thus, net margin was also lower year on year at 22.4 percent versus 26 percent in CY17.

The company witnessed the highest growth in revenue at over 16 percent crossing Rs 6 billion in CY19. Of this Rs 6 billion, its flagship brand “Rigix” contributed Rs 1 billion. Rigix is an antihistamine that commands a market share of 17.5 percent. Topline was also supported by a one-time price adjustment allowed by the Drug Regulatory Authority of Pakistan (DRAP). Thus, the better prices allowed for better profit margins as is reflected by the slightly higher gross margin of 58.5 percent. This also translated into an improved net margin of 23 percent; however, the increase in net margin was marginal due to a relatively higher tax expense.

In CY20, revenue grew by 11 percent to reach Rs 6.9 billion in value terms. There was a 9 percent rise in the domestic portfolio, while export to Afghanistan registered an increase of more than 41 percent. The latter was a result of an agreement towards the end of CY19, the result of which is reflected in CY20. In CY19, the Afghan government had imposed heavy levies that impacted exports to the country. But due to currency devaluation, cost of production increased to 44.4 percent, causing gross margin to decline to 55.6 percent. However, net margin remained more or less flat at close to 23 percent due to reduction in finance expense. This was due to repayment of Sukuk, low interest and controlled utilization of running finance facility.

Revenue growth in CY21 was relatively subdued at 6.8 percent, to cross Rs 7 billion in value terms. While the domestic sales registered a growth of 14.8 percent, export sales declined by 22.9 percent, driving down the overall growth to 6.8 percent. Export sales were adversely impacted by political unrest and border closure in Afghanistan. However, there was nearly no change in gross margin that was recorded at 55.5 percent for the period as cost of production continued to consume 44.5 percent. While there was little change in other elements, administrative expense escalated to make up over 5 percent of revenue. This was attributed to payroll expenses and investment in CSR activities and donations. Thus, operating margin reduced from nearly 30 percent in CY20 to nearly 27 percent in CY21. However, the drop in net margin was slightly contained due to a further decline in finance expense.

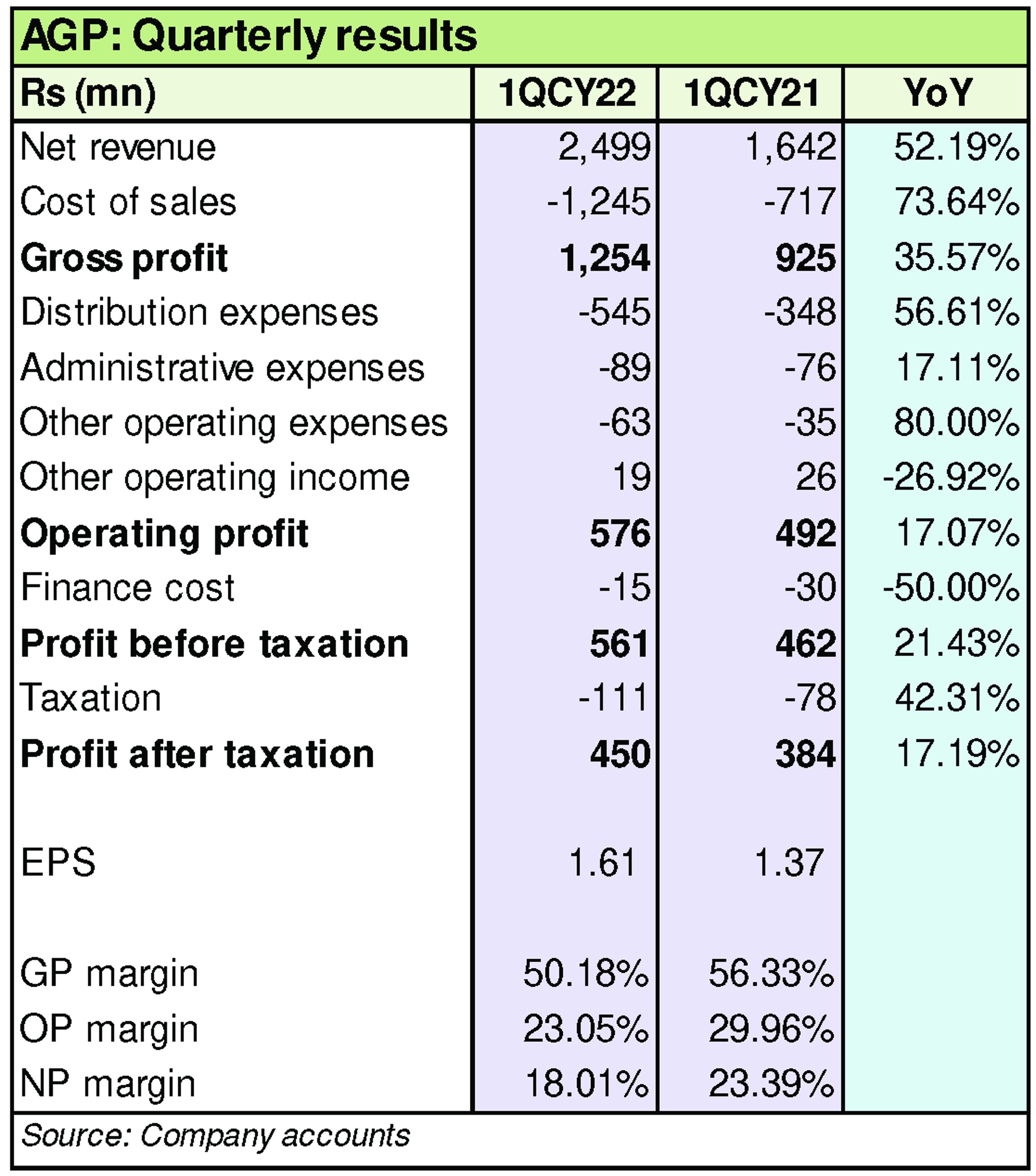

Quarterly results and future outlook

Revenue in the first quarter of CY22 was higher by over 52 percent year on year. At Rs 2.5 billion, it was the highest quarterly topline ever achieved. This was attributed to an increase in the domestic portfolio by 26 percent, while export sales to Afghanistan witnessed an increase of 30 percent year on year as the political situation stabilized. However, profitability was significantly lower year on year with a gross margin of 50 percent, compared to over 56 percent in 1QCY21 as cost of production consumed a higher portion of revenue. This was due to currency devaluation, inflationary pressure and logistical costs. This also trickled to the bottomline that was although higher at Rs 450 million versus Rs 384 million n 1QCY21, net margin was lower at 18 percent compared to over 23 percent in the same period last year.

The company has seen strong topline performance consistently since CY16 on the back of growing demand as well as operations. But with international commodity prices rising, and global financial conditions worsening, the country is also facing political and economic instability that can threaten the company’s future profitability.

Comments

Comments are closed.