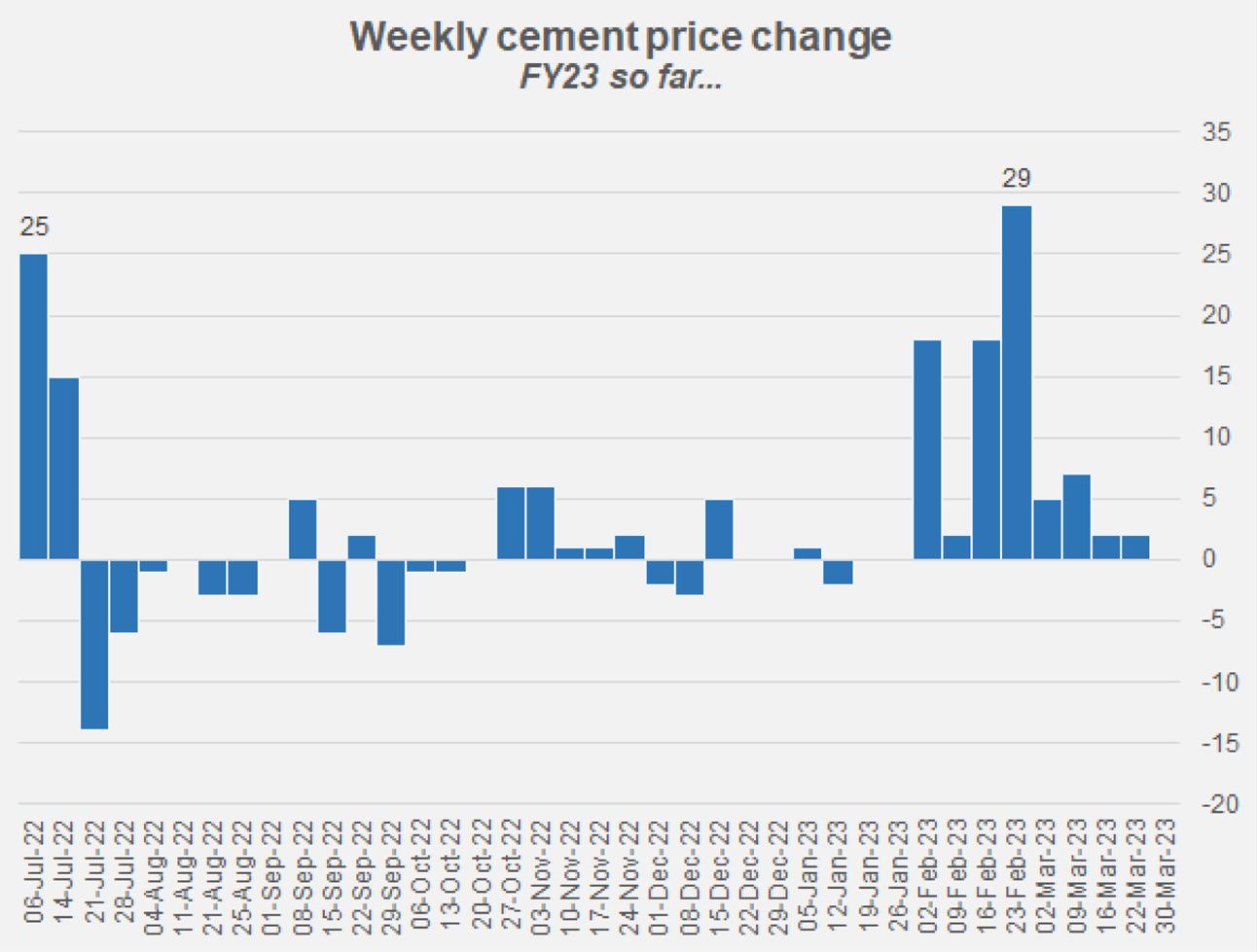

In the week following the government’s proposal to raise FED on cement and sales tax across the board, cement prices saw their highest weekly jump yet of Rs29 (on average across a variety of markets sampled by the Pakistan Bureau of Statistics). Between that and the first week of Feb-23, the total price increase for a 50-kg cement bag was as high as Rs100 in certain markets. In the South, prices have been less erratic with long stretches of no price changes, but bigger jumps visible when prices were raised. In contrast, prices in the north have increased consistently almost every 2 weeks starting with a big surge around July.

The indiscriminate rise in the cost of construction as a result of these price hikes has certainly dampened demand for cement and other building materials that have seen similar price trajectories. By Feb-23, domestic offtake for cement had fallen 13 percent (cumulatively since July) year on year, which compared to the average weekly price increase of 45 percent (year on year) is still fairly contained. Indeed, the average monthly domestic offtake for cement during this fiscal year so far (i.e. between Jul to Feb) comes to 3.4 million tons, or roughly 11,000 tons per day is still higher than FY17, FY19 and about the same as offtake during FY18 and FY20; though certain lower than the average monthly offtake of about 13,000 tons per day during FY21 and FY22. Capacities and effeciencies are also greater this year compared to previous years which has brought down utilization levels to about 55 percent.

However, cement prices have more than shielded manufacturers from watching their margins plummet in the face of falling demand. The other advantage has been utilization of coal sourced from local and Afghan suppliers. The industry was able to keep coal costs low as a result too when coal prices internationally were soaring, and these coal inventories also came to the rescue when import restrictions in the country caused massive supply chain disruptions for uninterrupted domestic production. As economic turmoil becomes malignant and spreads across all sectors of the economy, affecting firms and consumers alike, cement manufacturers are unlikely to lower prices over the next few months which inevitably will keep construction costs inflated. Ongoing private and public projects facing cost overruns will have to make tough decisions which may stall some projects and further reduce offtake. Hydropower construction projects are underway despite being hit by the floods, though cuts in PSDP disbursements will certainly trim down development demand consequently affecting building material sales.

Comments

Comments are closed.