National Refinery Limited (PSX: NRL) was incorporated in 1963 as a public limited company. The company was privatised in the year 2005. As per its latest shareholding pattern, 50 percent of the shares are held by the associate companies that include Attock Refinery Limited and Pakistan Oilfields Limited, both holding 25 percent each. The other significant shareholder is Islamic Development Bank Jeddah, holding around 15 percent of the total shares.

NRL is engaged in the manufacturing, production and sale of a variety of petroleum products. The refinery's key fuel products include motor gasoline, kerosene, JP-1, JP-8, Euro II grade HSD, LPG, furnace oil. Its other products include Naphtha that is exported, sulphur, base oils, asphalt and speciality products

It has three refineries - two lube refineries and one fuel refinery. The first lube refinery was commissioned in 1966 with designed capacity of 3,970,500 barrels per annum of crude processing and 533,400 barrels per annum of lube base oils. The project cost was Rs104 million at that time.

The second lube refinery was commissioned in 1985 and its designed capacity of 700,000 tons per annum of lube base oils was enhanced to 805,000 barrels per annum after a revamp in 2008. The total cost of the project was Rs2,082 million for the initial refinery and Rs585 million for the revamping.

NRL's fuel side refinery started operations in 1977 with designed capacity of 11,385,000 barrels per annum of crude processing with two phases of up gradation. The capacity after the second round of revamping stood at 17,490,000 barrels per annum of crude processing. The cost of the project commissioned in 1977 was Rs607.5 million, while the two enhancements totaled Rs673 million.

NRL is the only refinery producing LBO in Pakistan. Its BTX unit was commissioned in 1985 with design capacity of 180,000 barrels per annum of BTX.

Its latest addition has been that of the commissioning of HSD Desulphurization and associated units to produce EURO II specification HSD. The total cost of the project has been Rs26.82 billion. In the same year, NRL also commissioned its Isomerisation Unit (Naphtha Block) with a capacity to process 6,793 BPSD of light Naphtha into petrol with a total cost of Rs6.54 billion.

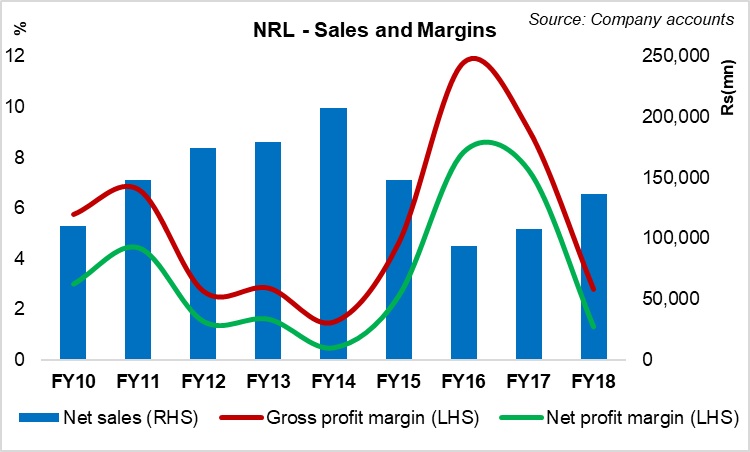

Past performance

NRL's revenues increased at an impressive rate from FY10-FY14, after which growth eroded due to falling prices of fuel products amid the supply glut as well as geo-political situation. However, margins seem to have taken a flight post FY14. The profitability margins were highest in FY15 as compared to the previous three years, which likely came from improvement in margins of refined fuel products versus crude oil. Lower prices of crude oil in FY15 helped the company invest unutilised funds to increase its interest income, and stable exchange rates during the latter part of the year also helped improve profitability.

NRL's lube segment has historically been more reliable in profit contribution as it is the only lube refinery in the country. The earnings of the segment improved further in FY16. The fuel segment after four difficult years turned profitable in FY16 versus loss in previous years. Improvement in profitability for NRL came from favourable margins between product prices and cost of crude and improved sales of HSD and Bitumen.

In recent years, NRL has also completed its project of self-power generation, which consists of two 7.2MW steam turbo-generator, a 4.0 MW diesel-FO engine power generator, and an 8.2 MW diesel-FO engine power generator.

In FY17, NRL commissioned its Diesel Hydro Desulphurization Project, within the assigned timeline of the government to produce low sulphur (EURO II Standard) High Speed Diesel (HSD).

During the year, NRL saw its revenues climb once again. However, the margins remained slightly lower than the previous year. The fuel segment profitability improvement came from improved margins in the international market as well as higher sales volumes by the firm. The net profit of the fuel segment for FY17 also included investment tax credit against investments in DHDS project. Profitability of the lube segment however, declined in FY17 mainly on account of higher feed cost and irregular increase in product prices.

FY18 Financial performance

In FY18, NRL's bottom-line fell by 78 percent, year-on-year, which was driven by losses incurred by the fuel segment in the fiscal year versus a profit in FY17. Though the revenues were up by 27 percent, year-on-year, the company's profitability was affected by higher operating cost including depreciation on new units, exchange loss, custom duty on crude oil, and lower return on bank deposits, according to the Annual Report. Also, increase in crude oil and product prices reduced the margins especially in case of fuel products. Besides, depreciation of the currency resulted in significant decline in profitability. These factors dragged margins; however, some respite came from elimination of price differential on HSD and higher revenue from increased production and sale motor gasoline - though these were not enough to contain the damage done by the higher costs.

The refinery segment witnessed depressed furnace oil sales. Whereas, the new units helped NRL to control losses a higher production of Euro II HSD and motor gasoline resulted in increase in revenue.

The firm's performance in the lube segment seems constant. However, decline in production was witnessed due to the turnaround of lube II refinery along with lower demand for lube base oil.

FY19 and beyond

In 1HFY19, NRL posted a loss of Rs3.86 billion versus a profit of Rs1.62 billion in 1HFY18. While the refinery depicted a healthy increase in net revenue, a key factor for the decline in profitability has been a more than proportionate increase in cost of sales. Higher cost of sales continued primarily because of higher crude oil prices, resulting negative gross margins.

The key challenge that NRL faces is the higher operating cost in shape of higher depreciation on the recently commissioned DHDS and ISOM units, and currency depreciation. The curtailment of furnace oil, and the refinery up gradations plans of the government have made the environment for refineries tough. Plus, the refineries might be in for some tough competition with UAE and Saudi refinery talks progressing quickly.

Comments

Comments are closed.