The latest financing scheme launched by the SBP targeting SMEs in Pakistan — a promisingly huge but historically underserved market for formal credit — does one crucial thing that gives the policy a compelling head start. It lures banks with competition, the seduction of which is much too great than any “mandatory targets” the SBP could thrust upon them.

The SME Asaan Finance scheme, also known as SAAF (clean) essentially invites bids from interested banks to attain a refinancing at 1 percent from SBP for three years (total Rs60billion available) for onward lending to SMEs at 9 percent whilst also offering a 60 percent risk coverage on loans that banks may underwrite free of collateral. Eight out of 20 banks including Habib Bank, United Bank Ltd, Allied Bank, Meezan Bank, Bank Alfalah, Bank of Punjab, JS Bank and Bank of Khyber have now been selected based on the amount of financing they will disburse and the number of borrowers they would reach.

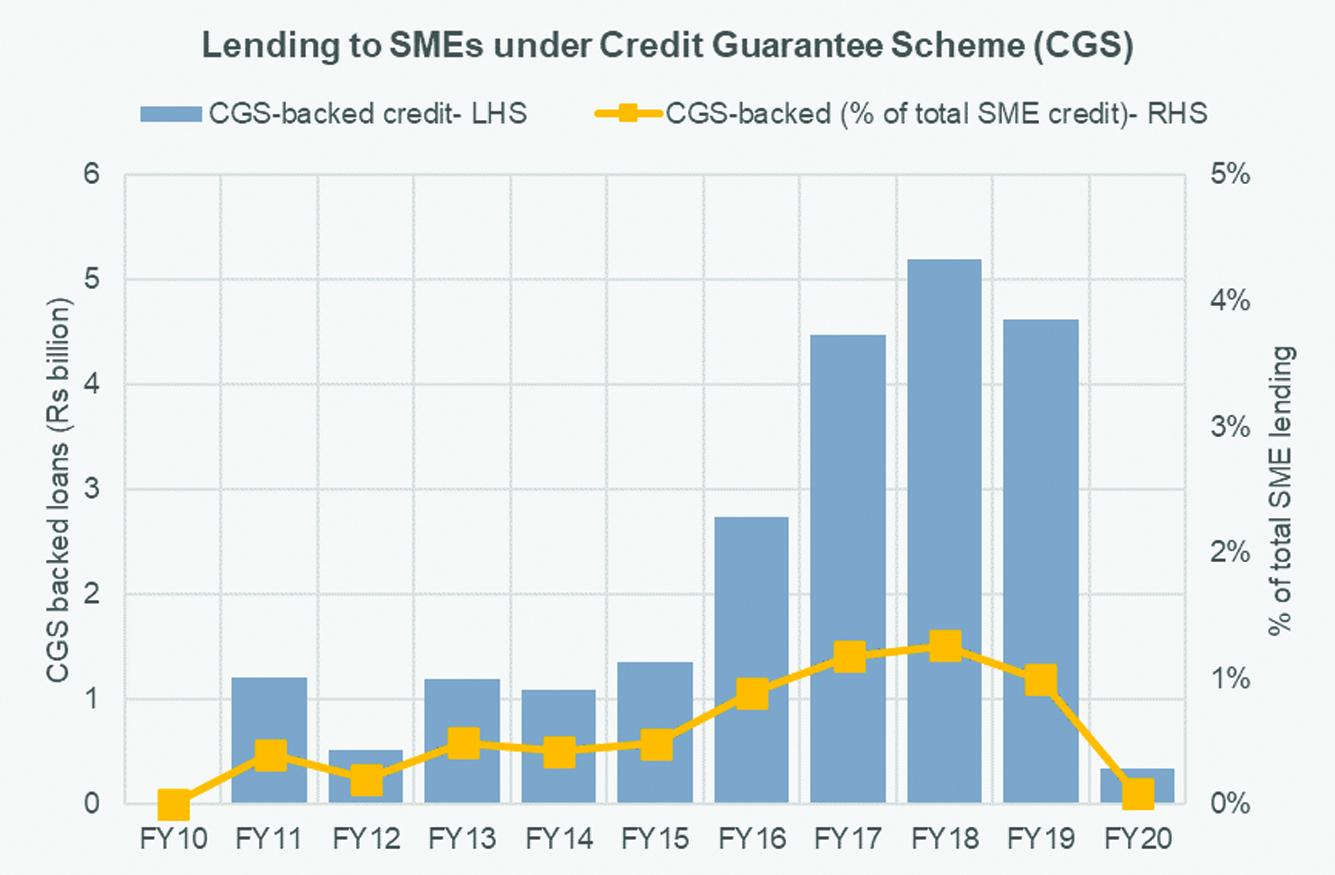

This is not the first time a credit guarantee scheme was announced. In 2010, the SBP together with funding from DFID launched a similar credit guarantee scheme (CGS) that had nearly no significant impact on total SME lending in the country (see graph). The scheme itself was redesigned several times during its course and many of its targets such as achieving 10 percent under-collaterized lending in total SME lending supported by government guarantee were eventually considered unachievable and replaced with other targets. Lack of adequate collateral has always hindered SMEs from attaining formal financing where adequate immovable collateral remains the major risk assessment requirement for banks. Banks have steered clear of SMEs due to the heavy burden they must bear when lending to this category. High infection ratio among SMEs when the economy was tanking has been historically lethal for them, but in general, SME lending also has higher intermediation costs (given their smaller loan size) with the current model of relationship-based lending simply making SME loans commercially unviable. The resources required to conduct a credit assessment for largely informal SMEs which also are collateral deficient has been too big an ask, unless they are properly motivated.

The CGS launched with DFID had a very lukewarm reception. In the start, banks stayed back as they were just coming out of a financial crisis and SME lending had burnt its bridges with them due to the legacy of previous toxic assets. Even with 60 percent guarantee coverage, the loan sizes were too small to justify the administrative costs associated to new borrower intake. The SBP had also put a cap on interest rates that banks could charge which they found to be overly prescriptive. The interest rate cap was eventually removed that piqued some interest, if not a lot.

Within that scheme, the degree of guarantee coverage was also linked to the level of collateralization such that 60 percent coverage was given to clean lending, 40 percent to loans where collateral was up to 100 percent of the loan value and only 20 percent coverage was given to loans where collateral value exceeded the loan amount. This incentivized under-collaterized or deficient collateral lending, though banks were not entirely sold on the idea.

Banks have traditionally relied far too heavily on immovable collateral and in most cases, their loan to collateral value for SMEs exceed 100 percent. Given SMEs lack of capacity to maintain their books in order, their inability to demonstrate business history and acumen, many operating in the informal sector made banks reticent. There were also no private credit bureaus that would conduct the necessary checks.

There has been some progress on that front. With the establishment of a Secured Transactions Registry, banks have become more open to lending to SMEs against charges on movable assets such as machinery, vehicles, plants, accounts receivables, gold etc. This has not completely eliminated banks’ reliance on immovable collateral but has to an extent bypassed that need, especially for smaller loans.

The only sure fire way to boost undercollaterized or clean loans among SMEs is through tech-driven credit scoring models which would require banks to make necessary investment in technology and/or partner with data aggregators and specialized fintechs that could underwrite the loans for them, or help them to do so. A number of fintechs have recently emerged that are loan targeting micro and retail enterprises and have already been fairly successful in bringing a large number of retailers and MEs on board. While they have been operating their models through partnerships with banks, many are now seeking a digital banking license. This is too big a market to not tap.

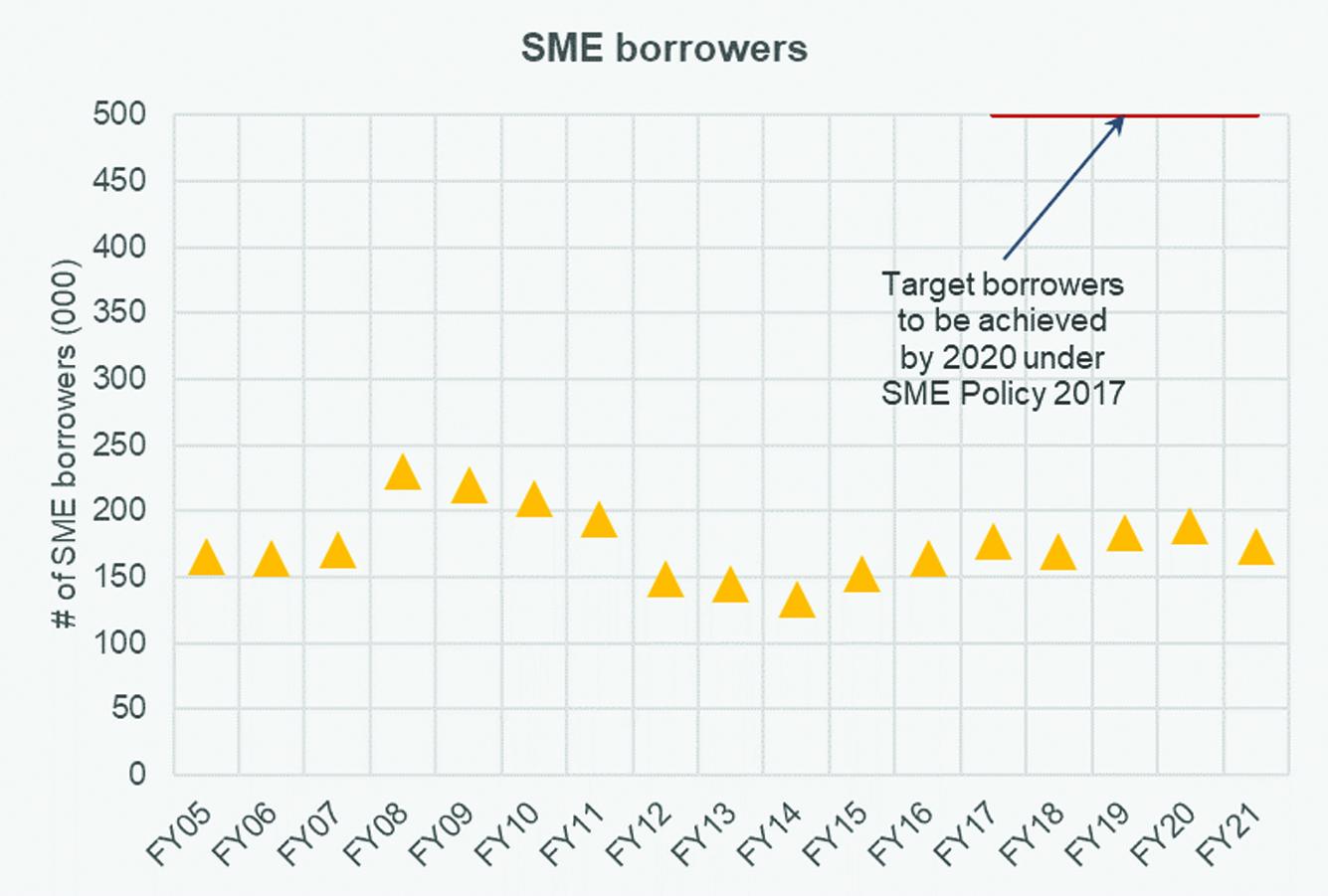

In 2017, the SBP came out with a SME policy that hoped to increase SME borrowers to 500,000 by 2020. The country is not even close to meeting that target because there hasn’t been a persuasive enough case for SME lending, given banks traditional comfort portfolios in corporate and government securities. This scheme could give that push to banks with the current combination of refinancing and guarantee coverage.

However, without spending on the right technology and developing modern systems, it would be nearly impossible for banks to gather a critical mass of new SME borrowers beyond this scheme. This is also why it was important for this scheme to have only the self-motivated banks on board that understand the sheer size of the SME market and the prospects of tapping it on their books.

Comments

Comments are closed.