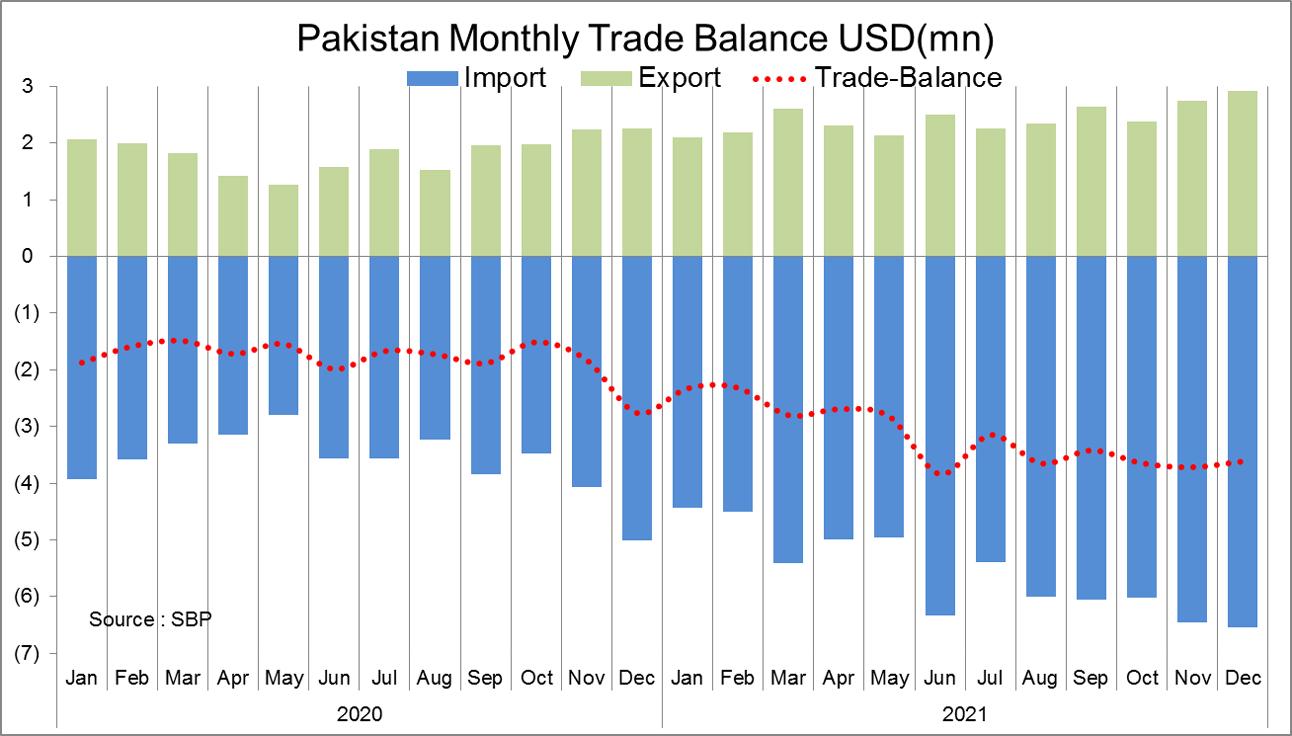

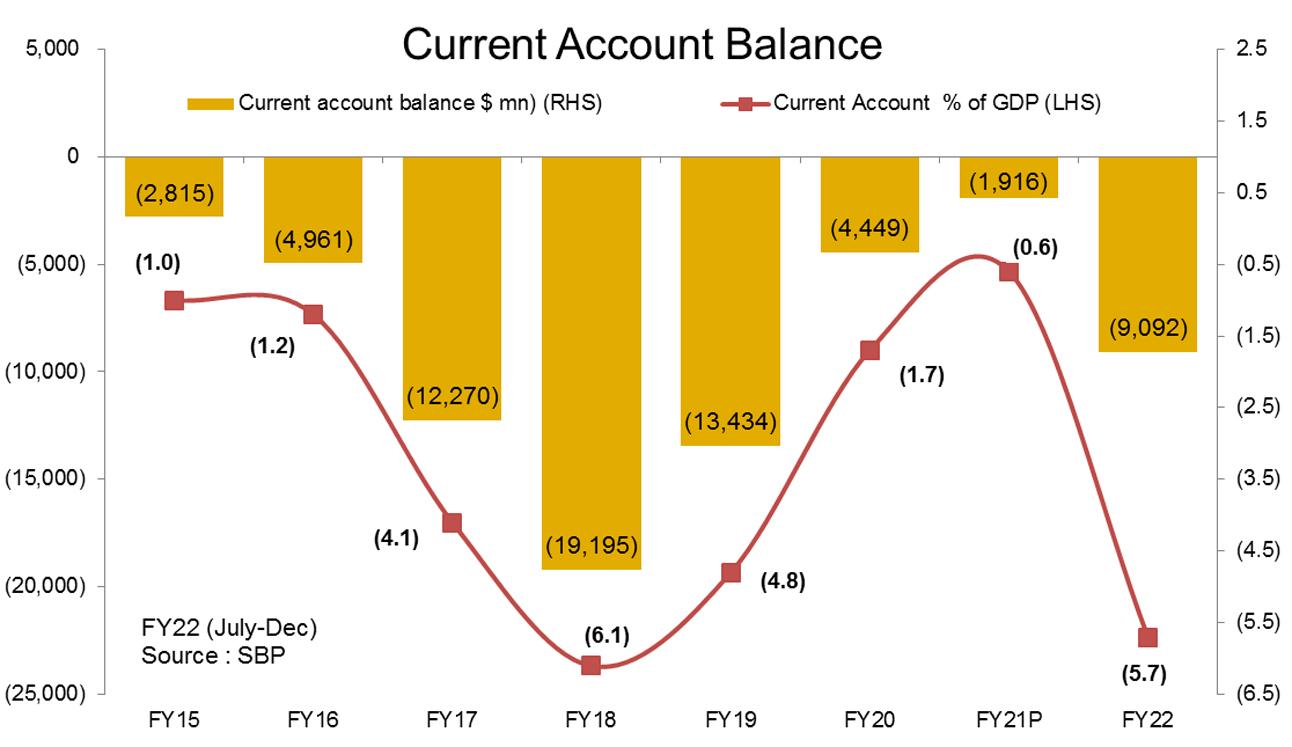

The current account deficitis growing again. It stood at $9.1 billion in the 1HFY22 – it’s the worst half since 2HFY18. Higher commodity prices -across the board and pick in the economic demand are some of the reasons for growing deficit. Both goods imports ($36.4 bn) and exports ($15.2 bn) were at all-time highs during the last half year. It’s a good omen as growing trade balance is depiction of growing economic activity.

The problem is that the quantum of imports is too high. Its up by 57 percent to $36.4 billion in Jul-Dec 2021. Imports based on PBS data is $40.6 billion. The gap is of 12 percent. There is a usual gap between PBS and SBP imports and that averaged at 6 percent during the first half of last ten fiscal years. Higher gap this year is due to higher value assigned to donated vaccines and some irregularities in the oil import bill, both recorded at PRAL. SBP numbers are based on payments and no payments have been made against PRAL’s arbitrary entries. That is why SBP’s imports are relatively lower and current account is milder than what many thought it would be, seeing averaging $7.8 billion monthly imports based on PBS data in Nov and Dec 2021.

The current account stood at $1.9 billon in Dec. The toll was same for Nov. Import bill came at $6.6 billion – inched up by 1 percent compared to the previous month. In 6M, the bill is up by 57 percent. Food imports are up by 28 percent in 1HFY22 to $4.2 billion. The biggest item – palm oil witnessed highest increase – up by 60 percent to $1.7 billion. Palm oil prices are trading at 10-years high which is driving imports growth.

Machinery imports are up by 24 percent in 6MFY21 to $4.8 billion and that is one of the drivers of imports. Thanks to TERF, many industries have expanded. Top on the list is textile – its machinery imports are up by 121 percent to $676 million in Jul-Dec. The growth in textile machinery is likely to generate higher export volumes in days to come. Mobile phone imports tapered a bit from a high base – down by 8 percent to $926 million in 1HFY22.

The heating up is in the transport sector where demand of vehicles is reflecting in imports figure – up by 88 percent to $1.9 billion in Jul-Dec 2021. Imports of cars, buses and other vehicles have seen some good growth. Lion’s share is of CKD cars – up by 117 percent to $836 million. The plethora of new SUVs being launched here are adding bill to imports. Approximately 10-15 percent of an average car’s value (before government taxes) is imported in the form of CKD kits or raw material/components for parts manufacturing.

The petroleum group is big and growing into a monster. Its toll has doubled to $8.6 billion during 1HFY22. Last year witnessed an exceptionally low number due to low oil prices, the toll this year is even higher than 1HFY18. Oil prices are hovering around 7 years high and LNG prices have gone crazy lately. The increase is across the board.

Agriculture and chemicals imports are up 41 percent to $5,280 million in 1HFY22. The most notable increase is in plastic materials which is up by 52 percent to $1.6 billion. PBS data suggests that there is marginal decline in material volumes. But the value has soared. Fertilizer and many other chemical prices are easily at their decade high. That explains the growth.

The story of metal group is similar. The toll is up by 54 percent to $3.1 billion in 6MFY22. Aluminum, copper, iron ore and other metal prices are either at or have recently touched 10-year high levels. That price effect largely explains the import growth. Food, oil, chemicals, fertilizer, and metals prices, all are at muti-years high. They all have their own cycles but since the pandemic led volatility has caused simultaneous peaking. The import bill shall remain high till commodity prices remain high. There is a limit of demand tightening. Nonetheless, recent monetary tightening and some increase in interest rates shall help shrink the import bill marginally.

It is heartening to see exports growing – up by 29 percent to $15.2 billion. Textile exports group is the greatest and has recorded the highest increase. It is up by 34 percent to $8.9 billion. This is due to combination of higher volumes and better pricing. The Cotton A index too is at its 10 years high and that is helping textile exports grow. Higher commodities have some positive impact too. But the volumes are higher in imports and that is why trade deficit is growing – the good trade deficit is up by 86 percent to $21.2 billion in 1HFY22.

Export services are growing good – up by 20 percent to $3.4 in 6MFY22. IT exports are going up. But with travel opening, import services are moving too – up by 39 percent to $5.3 billion. Overall goods and services trade deficit has worsened by 87 percent to $23.0 billion.

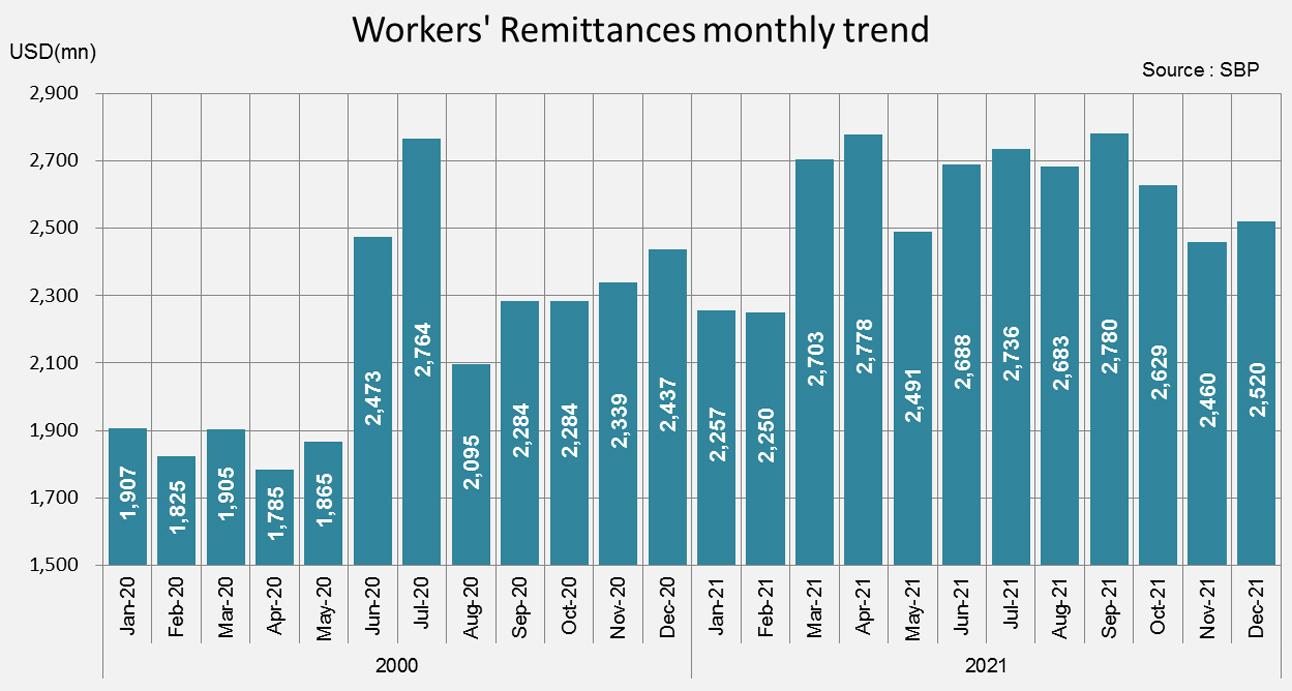

Worker remittances have remained resilient. These keep on growing at a higher base even though number of new employees going abroad is on a decline. The toll is up by 11 percent to $15.8 billion. There is significant decline in other current transfers – down by 72 percent to $583 million in 1HFY22. Last year was exceptionally good as many charities and donations came through. These are tapering off now.

All these factors combined are causing slippages on the current account front. And taming the CAD is the worry SBP has today as it is imperative to preserve thin layer of foreign exchange reserves. Seeing the uptick in the deficit, the monetary policy hawks increased the policy rate by 275 bps to 9.75 percent in the last four months. Another policy announcement is due today. Expect no change. The SBP shall wait for inflation and current account during February before making a call for increase in March 2022.

Comments

Comments are closed.