Pakistan’s cotton imports are on the rise again.After importing just 3.1 million bales (of 170kg) during first nine months, over 1.1 million bales made their way through ports of entry during April and May 2022. At this rate, the fiscal year may now close with imports of 4.5 million bales, and an import bill of over $1.9 billion, highest ever in country’s history.

Although initial forecast for now closing trade year (2021-22) placed imports at 5 million bales, demand for foreign cotton slowed down significantly during the Jul – Dec ‘22. This was driven in part by upbeat trend of local cotton arrivals, which rose from 7 million bales during FY21 to 8.3 million bales by season end. Meanwhile, a surge in international prices by 54 percent on average also slowed down demand for upland and other imported varieties.

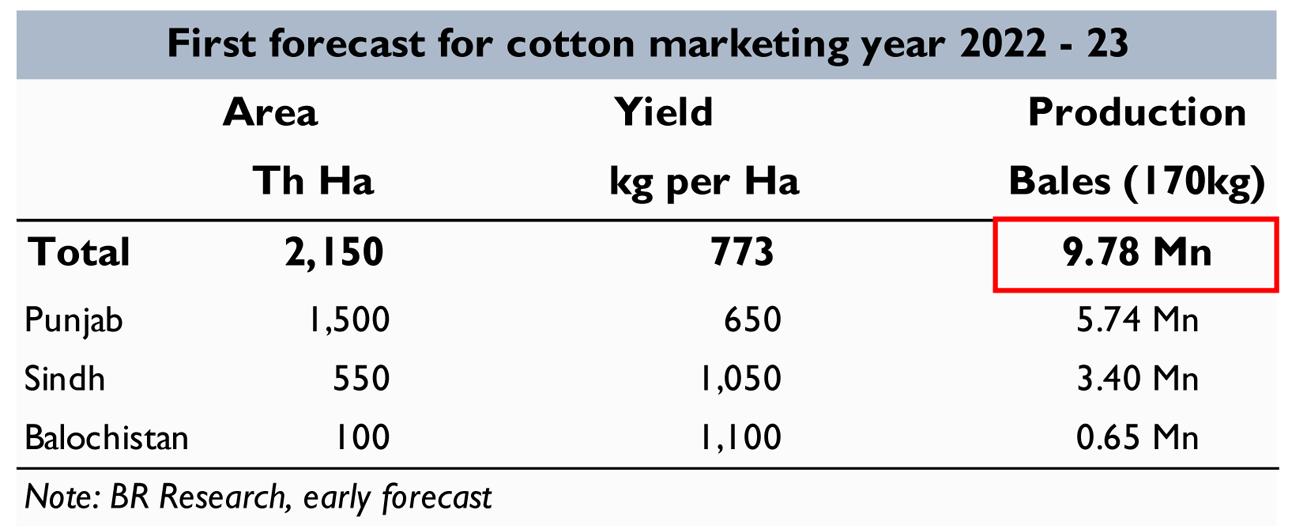

Which makes the current surge all the more surprising. The next cotton harvest season is just months away now, with a projected 10 percent rise in area under cultivation during kharif 2022-23.Although cotton acreage would still be third lowest in 40 years, the rise in acreage may help add 1.5 million bales in output compared to last year.

At a time when global commodity prices are significantly higher than local cotton, a revival in demand for imported raw material appears counter intuitive. One explanation, of course, is that the local textile industry anticipates significant rise in export orders, where demand may outstrip supply despite a projected rise in local output.

However, both global and local economic outlook negate this hypothesis. One, inflationary pressures in developed economies have made it ever more likely that exporting destinations may soon trigger a recession to curtain inflation, bringing down demand for discretionary spending precipitously. On the other hand, the political economic havoc over the last four months has made it nearly certain that local consumers will soon tighten the purse strings, bringing an abrupt end to Pakistani love for lawn and suits.

If these risks materialize, it will the worst possible outcome for revival of local cotton production. Either a demand-side slowdown, or an oversupplied local market will eventually lead to a downward spiral for local cotton prices come September 2022. Already, low yields and volatile weather means farmers still willing to risk growing cotton hardly manage to match the earnings of substitute crops. If cotton prices also crash, they will have little reason left to stick with the crop in coming years.

Higher cotton output – c. 10 million bales - in the upcoming harvest season may be a good omen for CAD fears, as it shall lower import bill by $0.25 - $0.5 billion for FY23. However, given demand-side risks of slowdown in exports, poor profitability or losses will most certainly drive farmers away for good.

Comments

Comments are closed.