MLCF: “Super” bad luck

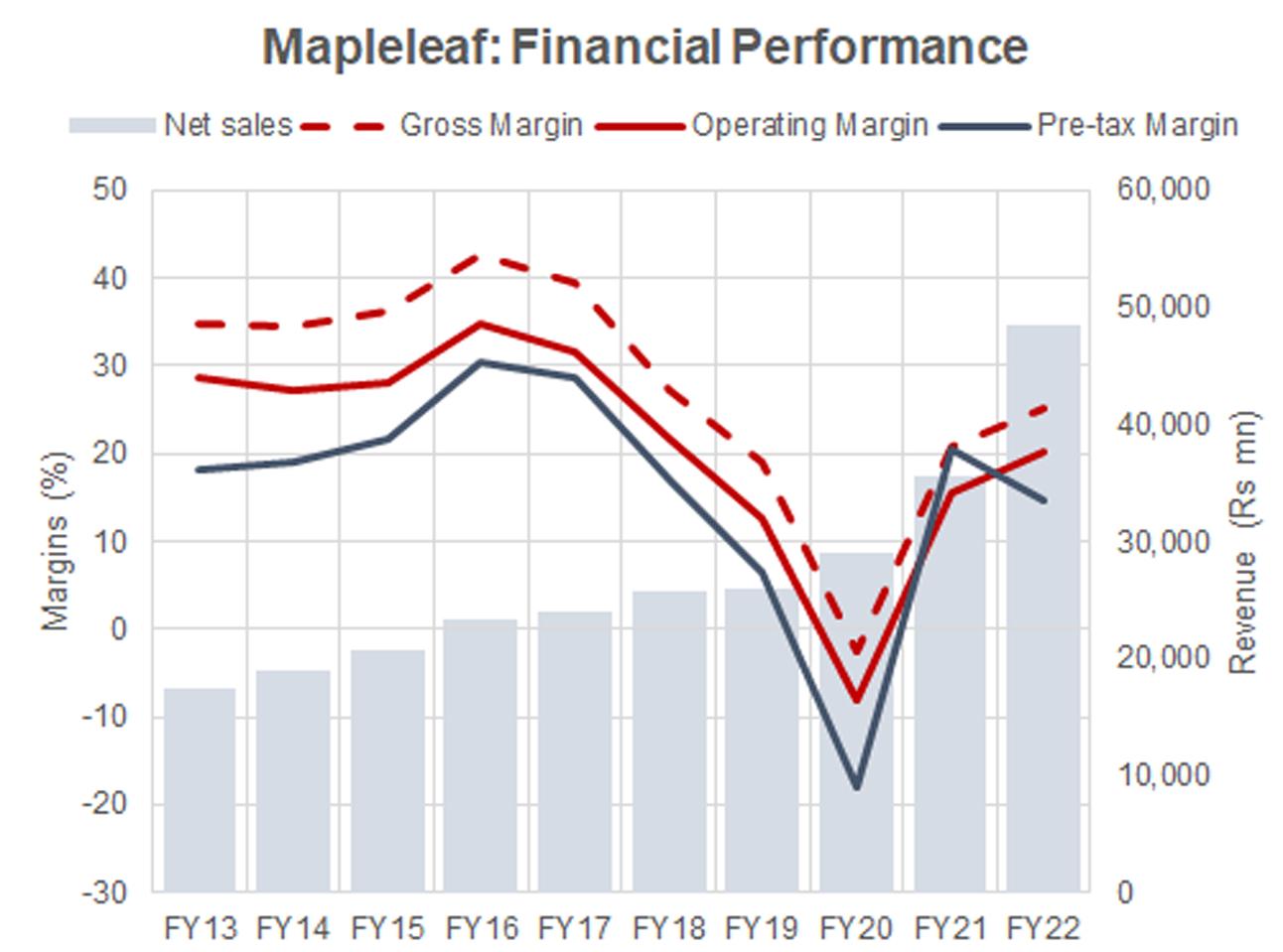

The fiscal year has not been kind to cement companies. Despite considerably better retention prices in nearly all northern markets, posting a top-line growth of 37 percent for the year and showing an improvement in gross margins during a very tough year from the perspective of costs, Mapleleaf Cement (PSX: MLCF) recorded a decline in earnings due to similar expense patterns as last year, a drop in other income and a last-minute government slapped super tax that could the tax incidence to 50 percent for the company.

As construction costs have risen, the demand for cement in the market for construction materials such as cement has been lacking in lustre both from the public and private sector with housing evidently not picking up despite the mark-up scheme under Naya Pakistan Housing Program (NPHP). To add insult to injury, for companies operating in the north zone and exporting cross-border, export markets drying up made the blow from slowdown in domestic markets that much worse. Mapleleaf’s nine-month exports fell 63 percent from Afghanistan becoming a difficult market to penetrate given the political and economic unrest brought forth by the exit of the US troops leading to the suspension of formal banking channels and considerably economy slowdown.

The company has also had to contend with higher costs due to commodity prices rising in the international markets at the outset of the Russia-Ukraine war. Expensive fuel and power, higher costs of imports from abroad as rupee depreciated all caused costs to increase, with the dominant cost component being coal. Mapleleaf shielded the blow to its margins from coal price rallies by procuring locally and from Afghanistan at considerably cheaper rates. This kept margins strong despite the inflationary costs, helped further by improved retention. In 9M, revenue per ton sold grew 39 percent which was higher than the increase in costs per ton sold (31 percent).

However, overheads and financial costs persisted at 7 percent and 4 percent of revenues, respectively, same as last year while “other income” that was 51 percent of before-tax earnings last year dropped to 1 percent. This led to a negative growth in before-tax earnings as it is (at -1.5% year on year) worsened considerably by a higher tax incidence. The resulting earnings decline of 42 percent is a bitter pill to swallow.

Demand is not expected to bounce back very fast as austerity is the order of the day and construction slowdown is certain. Inflationary pressures on households will keep consumers at home looking to not make any large purchases which will keep the home construction market weak. Lower government spending on development and fiscal tightening are all indicators that cement will remain down on its luck for a little while longer.

Comments

Comments are closed.