Al Shaheer Corporation Limited

Al Shaheer Corporation Limited (PSX: ASC) was set up under the repealed Companies Ordinance, 1984, in 2012. The company sells different types of meat such as meat of goat, cow, chicken and fish. In addition to selling locally, it also caters to the global market, particularly the Middle East.

Shareholding pattern

As at June 30, 2022, the directors, CEO, their spouses and minor children own about 27 percent shares, within which the CEO, Mr. Kamran Ahmed Khalili is a major shareholder. The local general public holds over 43 percent shares, followed by nearly 12 percent shares held under the category of “others”. Modarabas and mutual funds, and insurance companies own 7 percent shares each, while the remaining roughly 4 percent shares are with the rest of the shareholder categories.

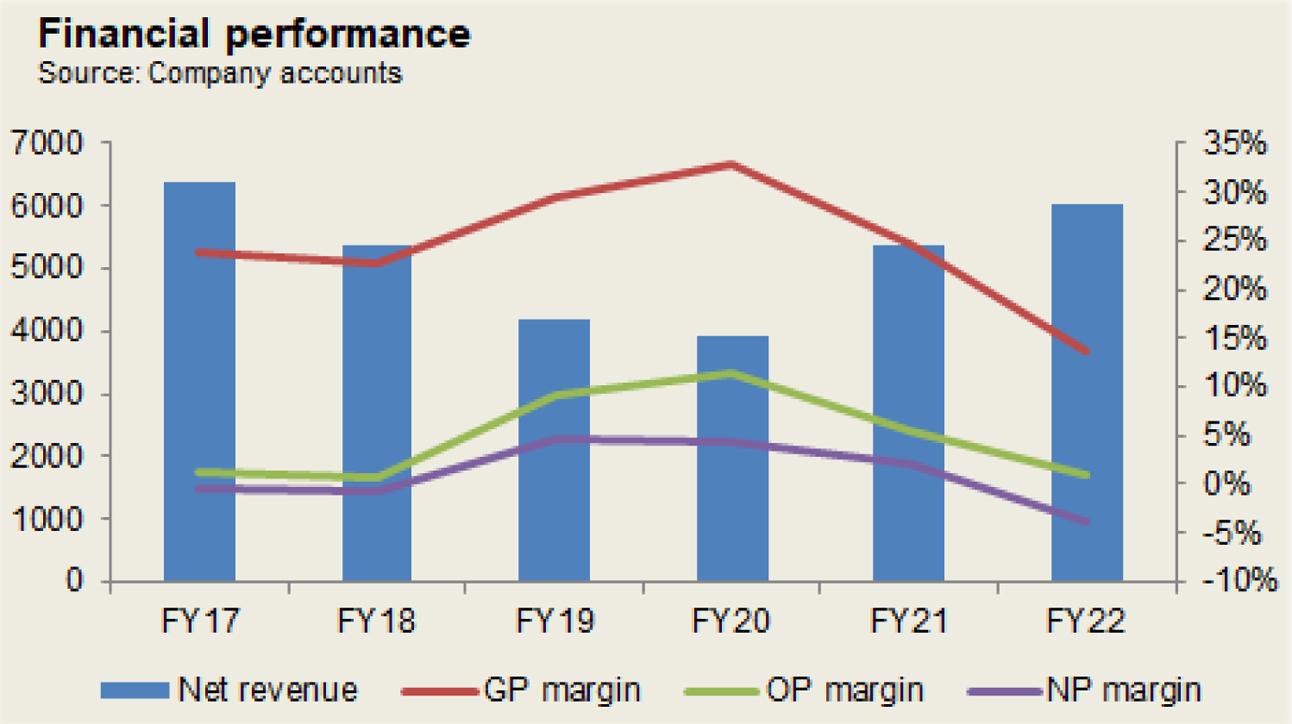

Historical operational performance

The company’s topline has been fluctuating, whereas profit margins, in the last six years have risen between FY17 and FY20, and declined thereafter.

In FY18, topline contracted by 16 percent for the second consecutive period. Exports fell by 25 percent, despite the currency devaluation that had benefitted export-oriented companies. This was due to cheaper alternatives available in the export destination markets, provided by countries like Brazil, Australia and India. The company’s production was also affected due to supply related issues. This too had an impact on sales. With a marginal increase in production cost, gross margin reduced slightly to 22.7 percent, from last year’s almost 24 percent. This also reflected in the net margin that fell to a negative 0.8 percent, compared to a negative 0.3 percent in FY17. The bottomline had received some support from other income that prevented a significant net loss.

In FY19, the company saw an even bigger contraction in revenue by 22 percent, with topline reducing to Rs 4 billion in value terms. Exports decreased by 7 percent, while the institutional sales net with competition from the unorganised sector. Moreover, the company also faced trouble at the cash flows end that was most probably the reason for lower cost of livestock purchases. Number of employees for the company had also reduced. As a result, cost of production declined to over 70 percent of revenue, causing gross margin to improve to 29.5 percent. Despite increases in other expenses and finance expense, net margin also improved to 4.56 percent for the year, as it saw notably higher other income.

Revenue continued to slide down, as it fell by 6.6 percent in FY20, with topline recorded at below Rs 4 billion in value terms. Sales in the first half of the year were lower due to Eid-ul-Azha, whereas sales in the second half were higher due to cash generation through rights issue, coupled with the outbreak of Covid-19 pandemic that increased the demand for clean and safe products. Thus, gross margin was recorded at an all-time high of 32.8 percent. However, net margin was flat at around 4 percent due to considerably lower other income and an escalation in finance expense. The latter consumed over 7 percent of revenue.

Topline in FY21 saw the biggest increase by over 37 percent with revenue increasing to over Rs 5 billion in value terms. Exports that had been on a decline for the last two years, registered a growth of a whopping 37 percent as the company chose sea routes during the pandemic that had created logistics issues. Sea routes also deemed beneficial in terms of cost as cargo cost decreased by 12.4 percent year on year. But the increase in prices of livestock drove cost of production higher to consume over 75 percent of revenue, reducing gross margin to 24.5 percent. But the decrease in administrative and finance expense as a share in revenue prevented net margin from falling drastically. It reduced to 2 percent for the year.

Recent results and future outlook

Topline in FY22 continued to grow, by 12.6 percent to cross Rs 6 billion in value terms. During the year, the company commenced production on its frozen and processed food facility in Lahore, particularly targeting the retail market. For the frozen food category, it focused on institutional sales. The institutional sales segment had performed incredibly well, increasing several folds year on year, despite the existence of competition from the unorganized sector. However, the inflationary pressure and the general macro environment factors led cost of production to increase to over 86 percent. Thus, gross margin fell to almost 14 percent. The company faced intense competition in the exports segment that impacted volumes and margins. This is reflected in the 8 percent decrease in exports. Despite significant support from other income that came from exchange gain, the company incurred the biggest loss seen since FY14, at Rs 239 million.

Presently, the company has been focusing on the retail market for its poultry and processed food segment; however, it aims to expand to HORECA and institutional sales.

office")

Comments

Comments are closed.