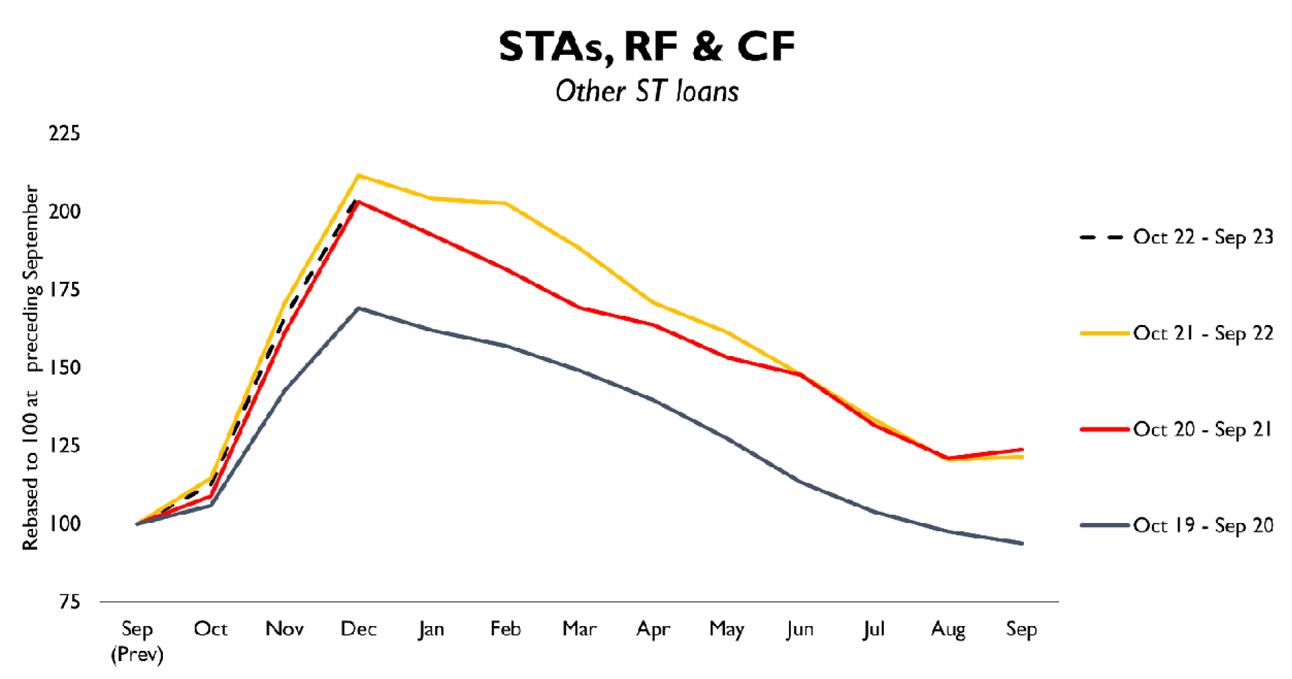

In its monetary policy statement announced on Monday, the State Bank of Pakistan (SBP) noted a “moderation in working capital loans to the private sector”. The rice processing industry –a subsegment of food product manufacturers - disagrees. According to the monthly disaggregated private sector credit snapshot published by the central bank for Dec 2022, rice market players have been borrowing like there is no tomorrow; as if the markup on loans has peaked at historic levels.

There is little by way of explanation to offer. USDA latest monthly update shows that the Ag-agency is standing steadfast with its initial prediction, forecasting national output of just 6.6 million metric tons (MMT) for the marketing year 2022-23, with 4MMT in exports. Yet, despite warnings of nearly one-third of national production being washed away, borrowing has followed in the footsteps of last year, when national production touched a record production of 9.3MMT.

In fact, based on SBP data, working capital lending to rice processors has effectively risen at the same pace as last year’s since the marketing season began at the end of Kharif 2022. By Dec 2022 close, working capital loans to rice processors rose by 62 percent over the Sep close (end of marketing year), against 65 percent during the corresponding period last year.

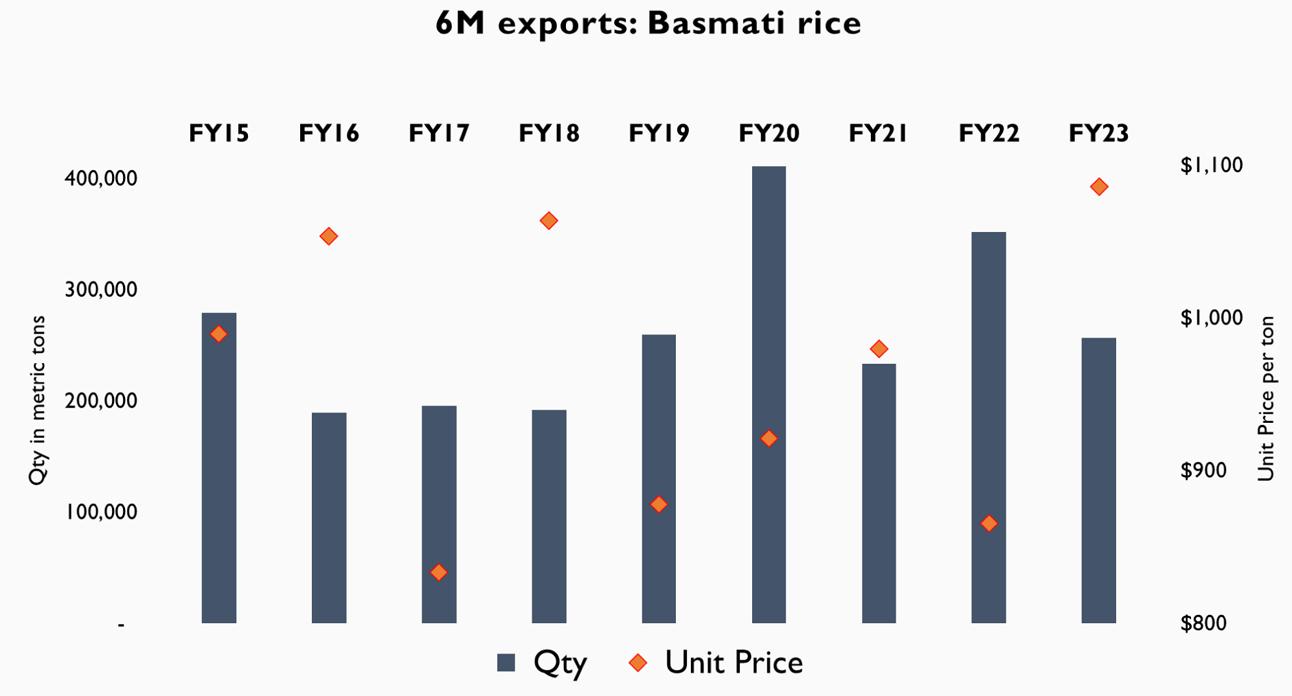

The rice export report card also offers little in the way of answers. Export volume declined at a record pace during 6M-FY23, falling by 23 percent over the corresponding period last year. Although basmati export volume has seen worse years, this is the first time in a decade that coarse rice exports suffered such a massive setback, which is in line with the destruction of the crop in the southern parts of the country. Total rice export barely managed 1.6MMT during 6M-FY23, against 2.2MMT in 6M-FY22. At this rate, USDA’s export forecast of 4.8MMT for FY23 appears to be a distant dream.

Significant support, however, was received by the upsurge in prices in the export market. Both basmati and coarse varieties averaged the highest unit prices in over a decade, muting the value impact of dwindling exports. Export revenue during the first half of the fiscal fell by just 13 percent year on year, raising hopes that two billion dollars in full-year export proceeds may still happen. Interestingly, however, the basmati export unit price fell during Dec 2023 despite the continued upsurge in the international market, giving credence to the theory that exporters are holding back on proceeds realization on account of anticipated depreciation in the currency.

With the weak export volume and even weaker supply, it remains unclear what’s behind the borrowing drive by rice processors. The margins in the commodity export market must be mouthwatering if market players are willing to make a play at a 20 percent borrowing rate, never mind the downside risk of a crash in international prices. Let’s see if the bet pays dividends!

Comments

Comments are closed.