Agriauto Industries Limited

Agriauto Industries Limited (PSX: AGIL) was incorporated in Pakistan as a public limited company in 1981. The principal activity of the company is the manufacturing and sale of components for motorcycles, agricultural tractors and automotive vehicles.

Pattern of Shareholding

As of June 30, 2023, AGIL has a total of 36 million shares outstanding which are held by 3,491 diverse shareholders. Foreign investors represent the largest shareholding category of AGIL holding around 42.24 percent shares followed by local individuals accounting for 34.34 percent shareholding in the company. Thal Limited which is an associated company of AGIL owns 7.35 percent of its shares while financial institutions have 7.12 percent stake in AGIL. Mutual funds and joint stock companies have a stake of 4.42 percent and 3.45 percent respectively in AGIL. The remaining shares are distributed among other categories of shareholders.

Financial Performance (2018-23)

Since 2018, AGIL’s topline has plunged twice i.e. in 2020 and 2023. Both were the times when the economy was passing through severe economic challenges that forced many businesses including AGIL to curtail their operations. AGIL also reported net losses in both these years. In the remaining years under consideration, AGIL’s topline has witnessed resilience and posted decent growth figures. However, in 2019 and 2021, AGIL’s bottomline also rode an uphill path while in 2022, it sustained massive decline. AGIL;s margins which had been narrowing down since 2018, registered staggering recovery in 2021 but the upturn couldn’t prove to sustainable as margins again assumed a downward journey since 2022 (see the graph of profitability ratios for a visual representation of AGIL’s margins). The detailed performance overview of the company is given below.

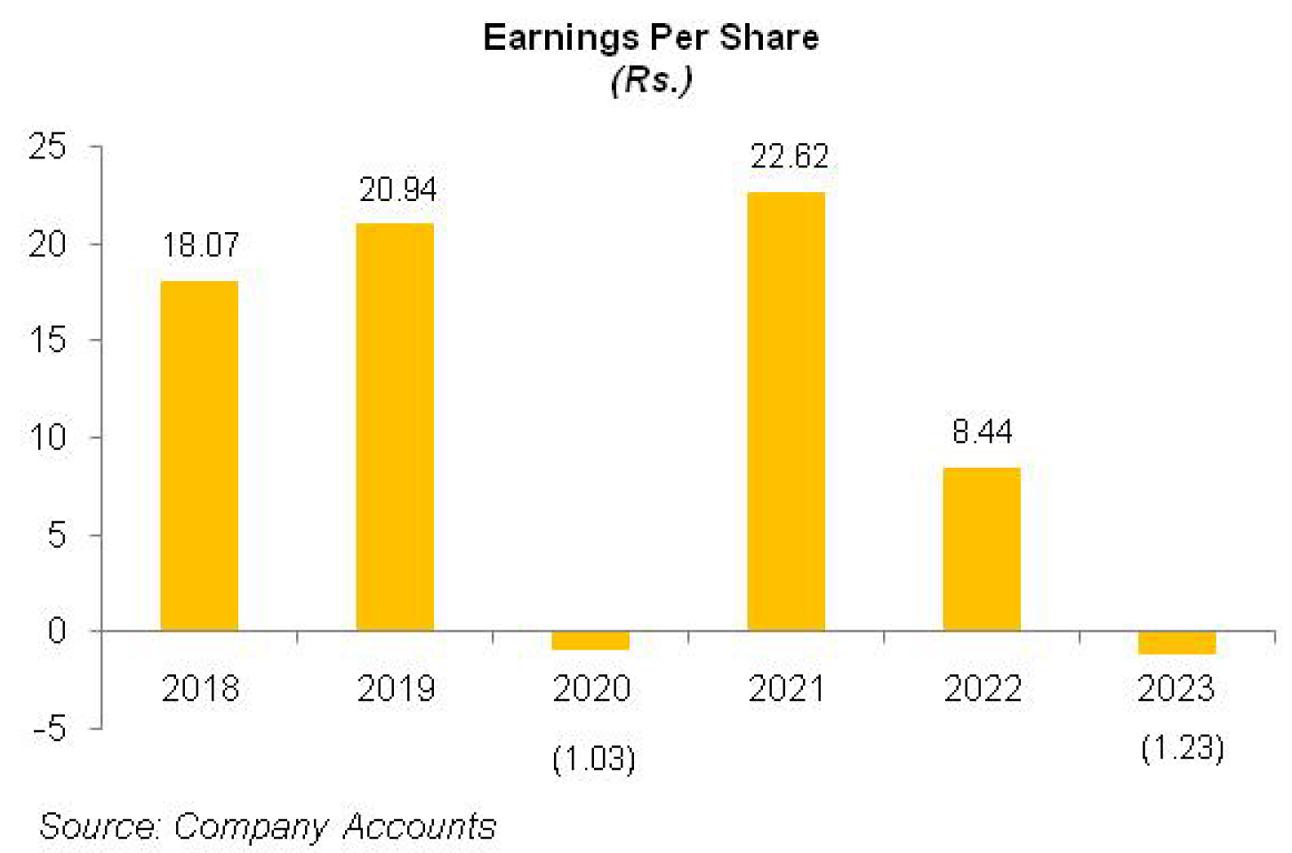

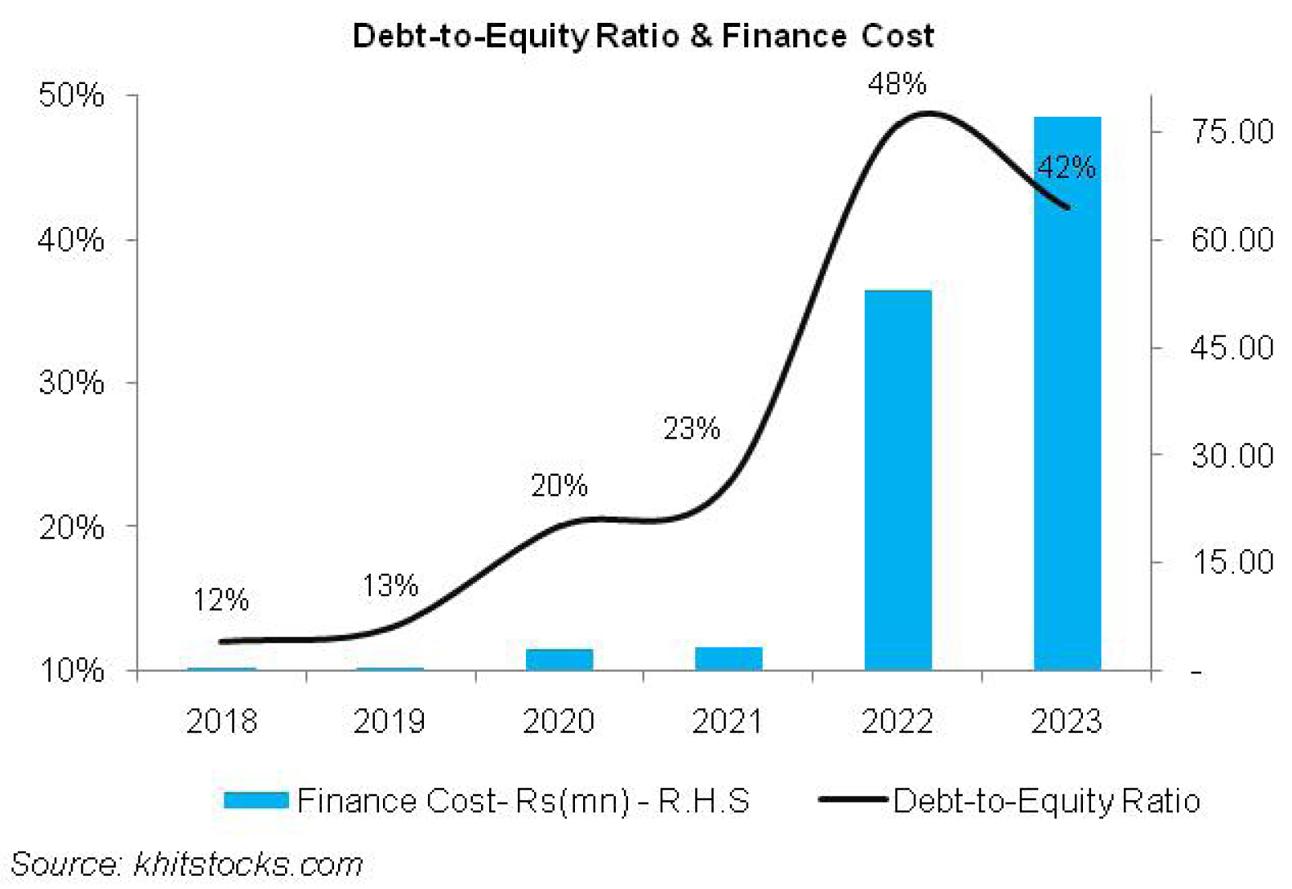

In 2019, AGIL’s topline grew by 17 percent year-on-year. This was despite the fact that the automobile industry witnessed considerable decline in volumes on account of upward price revisions, high cost of borrowing as well as tightening of imports. The same reasons also squeezed the gross profit of AGIL by 3 percent year-on-year in 2019 and pushed the GP margin down to 15.1 percent from 18.3 percent in 2018. Distribution cost grew by 8 percent year-on-year on account of high freight charges, advertisement and promotion as well as provision for warranty claims. High payroll expense also drove the administrative expense up by 10 percent year-on-year despite reduction in human resource tally during the year. AGIL recorded a net other income of Rs.84.16 million in 2019 as against the net other expense of Rs.16.49 million in 2018. This was primarily the result of hefty dividend income Agriauto Stamping Company (Private) Limited, the wholly owned subsidiary of AGIL. This significantly buttressed the operating results of the company and it registered a 4 percent year-on-year growth in its operating profit in 2019. However, OP margin fell to 11.3 percent in 2019 from 12.7 percent in 2018. The company was able to cut down its finance cost by 6 percent year-on-year in 2019 despite monetary tightening. It is pertinent to note that the company has not undertaken any external borrowings as its liquidity position is strong enough (see graph of liquidity ratios). The drop in finance cost was the result of a plunge in deferred taxation due to deductible temporary differences arising due to provisions. AGIL’s net profit grew by 16 percent year-on-year in 2019 to clock in at Rs.603.01 million in with an NP margin of 8.47 percent versus 8.51 percent in 2018. EPS also grew from Rs.18.07 in 2018 to Rs.20.94 in 2019.

In 2020, the local and global economy faced grave challenges on account of COVID-19. The global pandemic not only shook the wellbeing of people but also took a severe toll on business activity on account of lockdown as well as depressed demand. AGIL is no different as it topline slipped by 47 percent year-on-year as it felt the brunt of COVID-19 as well as decelerated performance of automobile sector on account of increase in custom duties, imposition of FED on locally manufactured vehicles and the restriction of sales to non-filers. Cost of sales also dropped, however, with a lower magnitude of 40 percent as the inventory levels rose resulting in high inventory holding cost. Moreover, Pak Rupee devaluation for most part of the year also inflated the cost. This compressed the gross profit by 84 percent year-on-year, with GP margin drastically falling to 4.5 percent in 2020. Distribution expense tapered by 45 percent year-on-year in 2020 due to considerably lesser advertisement and promotion campaigns assumed during the year coupled with lower freight charges on account of curtailed sales volume. It seems that the company laid off many employees during the year as it human resource tally declined from 709 in 2019 to 617 in 2020. This resulted in 1 percent lesser administrative cost incurred in 2020. AGIL booked a net other income of Rs.140.40 million in 2020, up 67 percent year-on-year which was the result of lower provisioning against WWF and no provisioning against WPPF and ECL. Despite a check on expenses, operating profit plummeted by 98 percent year-on-years in 2020 with OP margin doomed to 0.4 percent. Finance cost grew by 853 percent year-on-year in 2020, however, it still stays at a mere Rs.2.99 million, representing 0.07 percent of AGIL’s topline in 2020. The increase in finance cost was due to lease arrangements done by the company for its offices and warehouse. AGIL’s posted a net loss of Rs.29.798 million in 2020 with a loss per share of Rs.1.03.

2021 proved to be the year revival for AGIL and made up for its losses and dismal sales performance in the past year. In 2021, AGIL registered a splendid topline growth of 85 percent year-on-year. This was the result of staggering resurgence in agricultural and industrial growth in 2021. Favorable foreign exchange parity and low interest rate instilled growth in automobile sector. The government also provided tax reliefs on cars with low engine capacity of 1000 cc, resulting in 61 percent higher sales volume of passenger cars in 2021. Moreover, FED was reduced to 2.5 percent across all the car segments. The company kept a check on its cost which was supported by appreciation in the value of local currency. This translated into a 482 percent year-on-year growth in gross profit with GP margin jumping up to 14.2 percent. Distribution expense spiked by 64 percent year-on-year in 2021 due to rigorous advertising and promotion campaigns launched during the year coupled with high freight and forwarding charges. Administrative expense slid by 14 percent year-on-year due to considerably lower legal and professional charges incurred during the year. Employee tally grew to 727 in 2021. Net other income grew by 14 percent year-on-year on account of dividend income from its subsidiary. Operating profit multiplied by 6144 percent in 2021 with OP margin rising up to 12 percent. Finance cost grew by 5 percent year-on-year despite monetary easing due to increase in lease liabilities coupled with the attainment of short-term running finance in 2021. AGIL posted a net profit of Rs.651.40 million in 2021, the highest among all the years under consideration, with an unparalleled NP margin of 9.3 percent and an EPS of Rs.22.62.

In 2022, AGIL’s topline measured up by 29 percent year-on-year, however, it couldn’t trickle down into a bottomline growth on account of high cost of sales, elevated cost of borrowing, record inflation and drastic depreciation of Pak Rupee. The topline growth was the consequence of improved automobile sales during the first 10 months of FY22.on account of all-time high sales of passenger cars. Then SBP intervened and put restrictions on import of CKD units to safeguard the diminishing foreign exchange reserves of the country. This put a dent on the production and sales of automobiles towards the end of FY23. The cost of sales grew by 33 percent year-on-year on account of Pak Rupee depreciation and import restrictions which created supply chain impediments for AGIL. Gross profit inched up by 3 percent year-on-year in 2022, however, GP margin marched down to 11.4 percent in 2022. Distribution expense magnified by 15 percent year-on-year in 2022 due to high freight charges on account of increased sales volume and rise in the prices of POL products. Focused advertisement campaigns also contributed towards high distribution expense in 2022. Number of employees grew from 990 in 2021 to 1061 in 2022, resulting in higher payroll expense and administrative expense escalating by 24 percent in 2022. AGIL incurred a net other expense of Rs.131.48 million in 2022 due to massive exchange loss incurred on foreign currency transactions. Operating profit tapered by 39 percent year-on-year in 2022 with OP margin slipping to 5.7 percent. Finance cost hiked by 1593 percent year-on-year in 2022 as the company’s short-term financing greatly increased during the year and it also availed SBP refinance scheme for renewable energy. The bottomline declined by 53 percent year-on-year in 2022 to clock in at Rs.304.009 million with an NP margin of 3.4 percent and an EPS of Rs.8.44.

Recent Performance (2023)

The automobile sales which started dropping towards the end of 2022 worsened in 2023 on the back of import restrictions, tapering of auto financing due to high discount rate and also because of imposition of new taxes in the latest budget. The devastating floods in the 1HFY23 wreaked havoc in the agricultural regions and took its toll on the tractor sales. The sluggish performance of automobile sector had the direct negative effect on the off-take AGIL. Due to lower production, cost of sales also slid, albeit with a lower magnitude of 36 percent year-on-year. Gross profit measured down by 79 percent year-on-year with GP margin narrowing down to 4.1 percent. Owing to demand destruction, the company greatly reduced its advertising budget in 2023. This coupled with lower freight cost resulted in a 29 percent dive in distribution expense in 2023. AGIL significantly trimmed down the HR tally from 770 in 2022, however, inflation didn’t allow administrative cost to slide accordingly and it stayed almost at the same level as it was in 2022. As against 2022, when the company booked net other expense due to high exchange loss, in 2023, AGIL posted a net other income of Rs.162.81 million on account of encouraging dividend income from Agriauto Stamping Company (Private) Limited. However, this couldn’t do any good to the operating results of the company. Operating profit slid by 91 percent year-on-year in 2023 with OP margin drastically falling to 0.8 percent from 5.7 percent in the previous year. Finance cost escalated by 46 percent year-on-year in 2023 due to high discount rate coupled with increased long-term financing obtained under SBP refinance scheme for renewable energy. AGIL incurred a net loss of Rs.44.28 million in 2023 with a loss per share of Rs.1.23.

Future Outlook

The expected bumper crop will boost tractor sales in FY24. Tractor sales have already improved by 34 percent year-on-year in August FY24 on account of low-base effect due to floods last year. Moreover, the projected surge in demand of passenger cars and two wheelers in FY24 in quest of low cost commute amid high inflation and fuel prices will also buttress automobile sales in FY24. The improved availability of CKD units due to ease of import restrictions have resulted in enhancement in capacity utilization of auto industry. All these factors point towards improved off-take of AGIL. However, will the improved sales trickle down to produce a strong bottomline amid high inflation, Pak Rupee depreciation, heightened energy tariff and elevated cost of borrowing will be a real feat to witness.

Comments

Comments are closed.