National headline inflation has shown no signs of cooling off – inching up another 1.8 percent month-on-month in January 2024, at 28.3 percent year-on-year. The year-to-date headline inflation for seven months stands at 28.8 percent – having stuck around the same throughout the fiscal year. Mind you, this comes off a very high base of 25.4 percent in the same period last year. It has now been 20 straight months of national headline inflation staying clear of 20 percent year-on-year.

In a parallel universe, the central bank, in its latest monetary policy statement has continued to expect a “significant decline” in the second half, expecting FY24 average inflation in the range of 23-25 percent. Headline inflation will have to decline by 2 percentage points for each of the remaining five months of FY24 – and even then, the yearly average would be 26 percent.

It will take a never-before-seen rally of month-on-decline – as the sharpest fall in the last six years for a month was 2 percent – and there has never been an instance of five month-on-month decline in urban or rural CPI. It is safe to say inflation for FY24 will average significantly higher than the upper band of the revised SBP guidance – which will invariably lead to moving the short to medium-target target of 5-7 percent inflation – goal post by another quarter or two – for the umpteenth time.

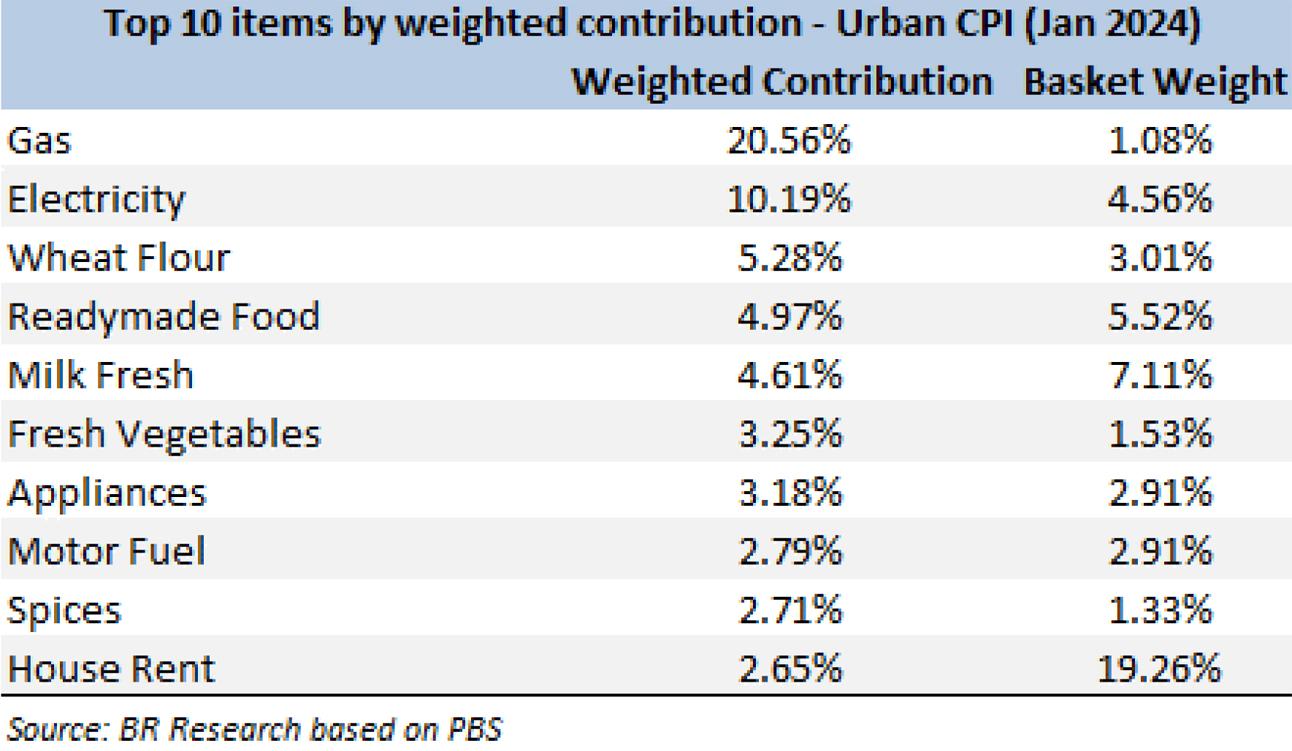

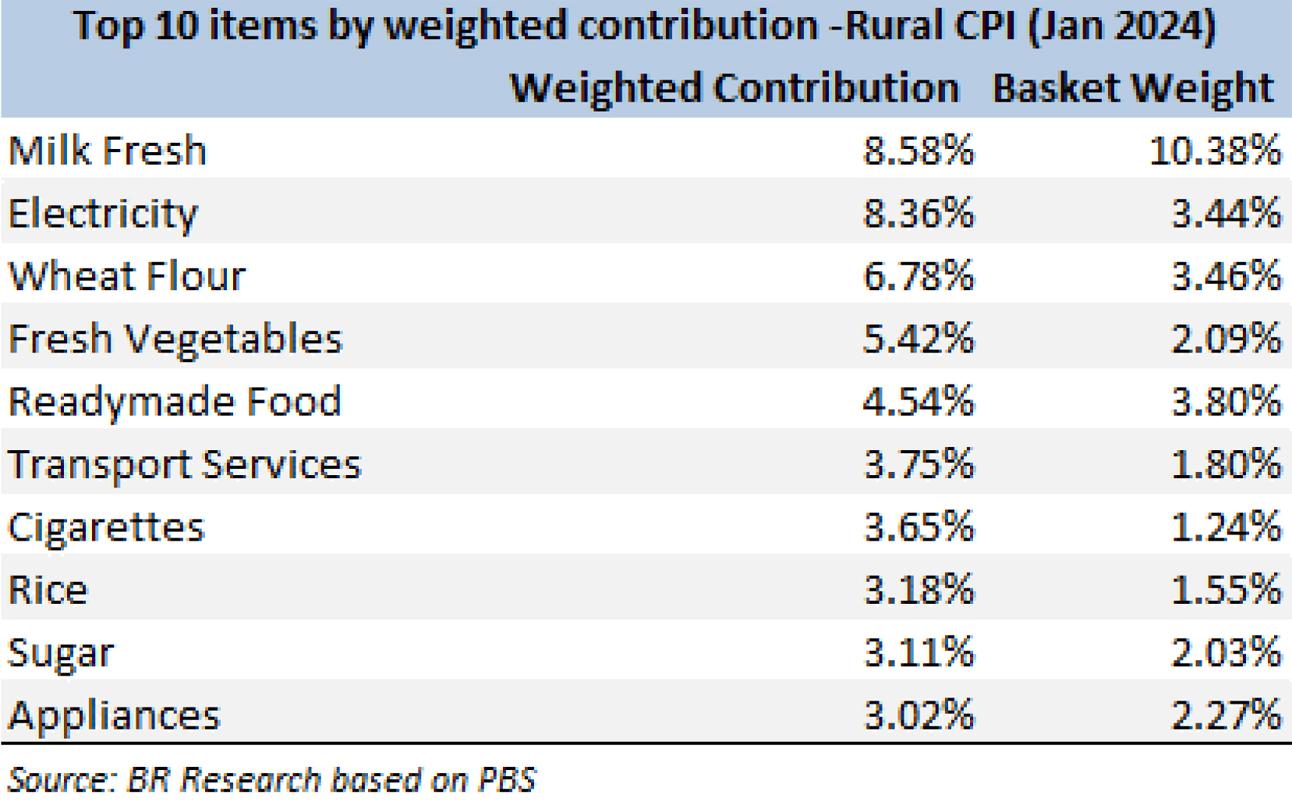

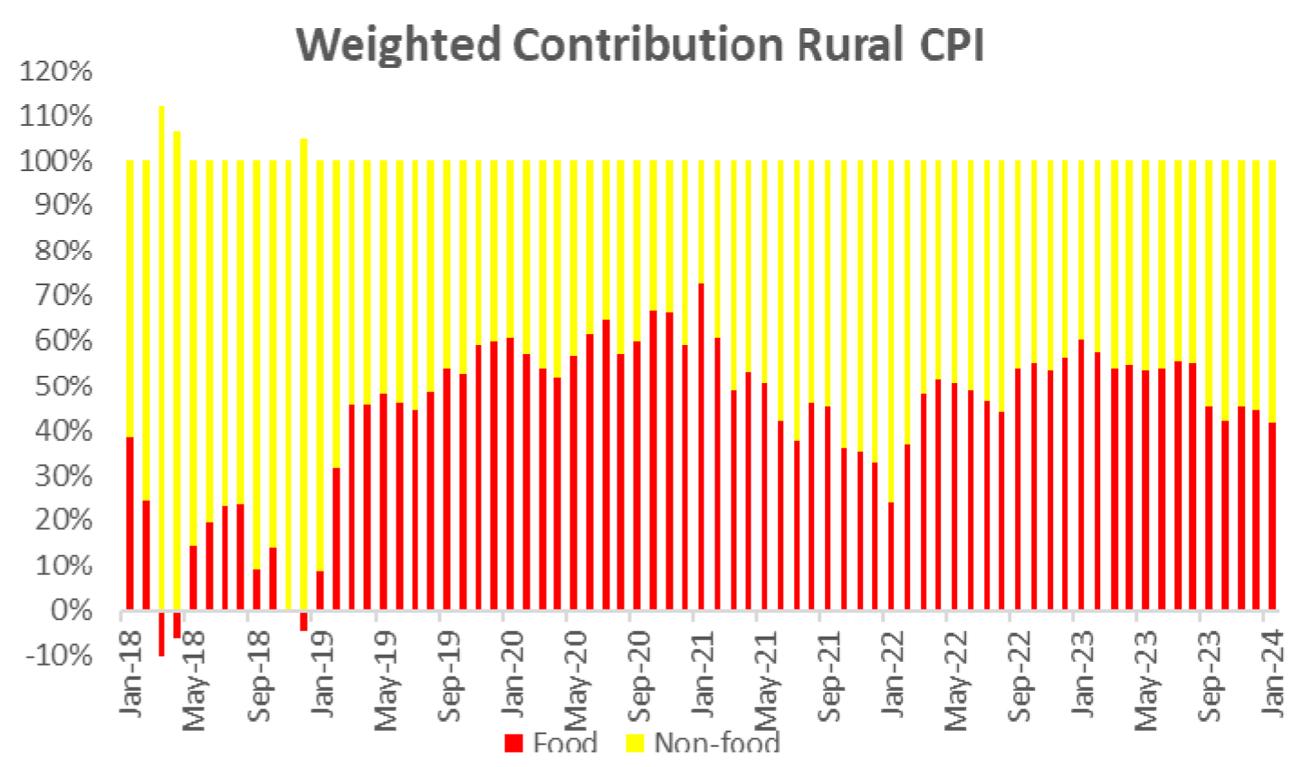

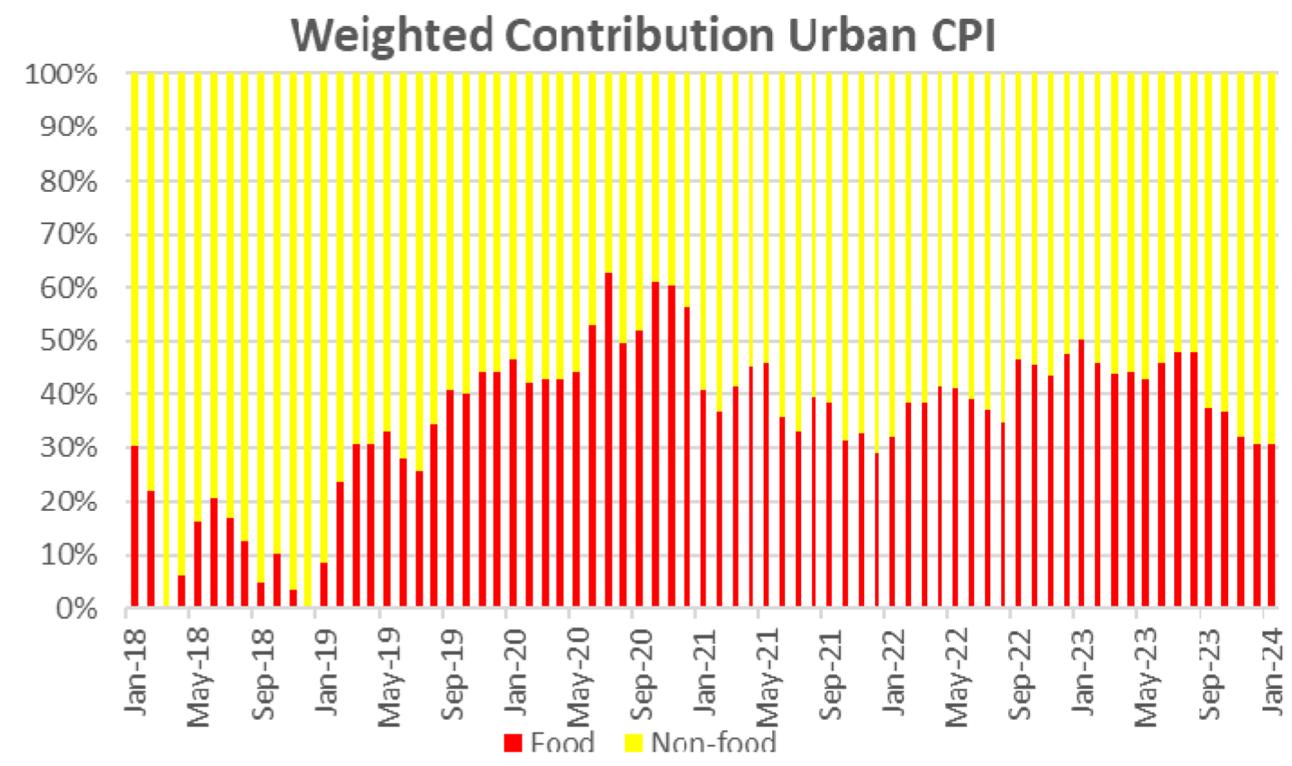

In terms of composition, the focus has gradually shifted from food to non-food – more pronounced in the rural setting, where weighted contribution of non-food items to inflation is 70 percent – matched only once since August 2019. Sharp adjustments in administered energy prices are at the core of headline inflation – with gas and electricity taking the top two spots in urban settings for weighted contributions – at 20 and 10 percent respectively, as against a combined weight of 5.6 percent.

All said, the PBS once again messes up with the treatment of electricity tariffs –showing a 6.4 percent month-on-month increase. The ground reality though, is much different as January 2024 saw the induction of another quarterly adjustment of Rs1.15/unit – on top of the existing QTA of Rs3.28/unit, as the former does not expire till March 2024.

Monthly fuel charges adjustment at Rs4.13/unit was also higher from Rs3.08/unit for the previous month. The unprotected category in fact faced an average 21 percent month-on-month increase – which accounts for a little over 50 percent of all consumption. The only slab that faced a lower month-on-month increase than what the PBS reported is that of 700 plus units. The PBS is expected to continue mistreating electricity tariffs. More sharp adjustments are already on the way – as a colossal Rs81 billion in lieu of QTA has been sought for 2QFY24. Monthly FCA for February will also be higher than the previous month. And then, gas prices face another upward revision under the IMF’s watchful eyes, which could come into effect as early as March 2024.

The core inflation has somewhat softened as the year has gone by – but the WPI stays heated, that is a telltale sign of another round of transmission to retail. The talks of inflation in teens anytime soon appear far from reality. The government has also agreed with the IMF to impose higher taxes on textile and sugar consumption in case of monthly revenue shortfall. January 2024’s FBR target was missed. Brace.

Comments

Comments are closed.