The verdict is in. After the great tumble of equities across the global earlier this week, commentators and pundits seem to be speaking in unison: Central banks across the world seem to have done too little, too late to curb pressures on global spending, and a global recession seems to be less than a quarter away, at least in developed, high income markets.

Whether it is the Sahm rule indicating labor market softening, or the 10-2-year Treasury yield spread, the alarm bells are ringing on recessionary headwinds gaining hold across the board. Meanwhile, the further heating up of conflict across the Middle East theatre certainly isn’t helping things either.

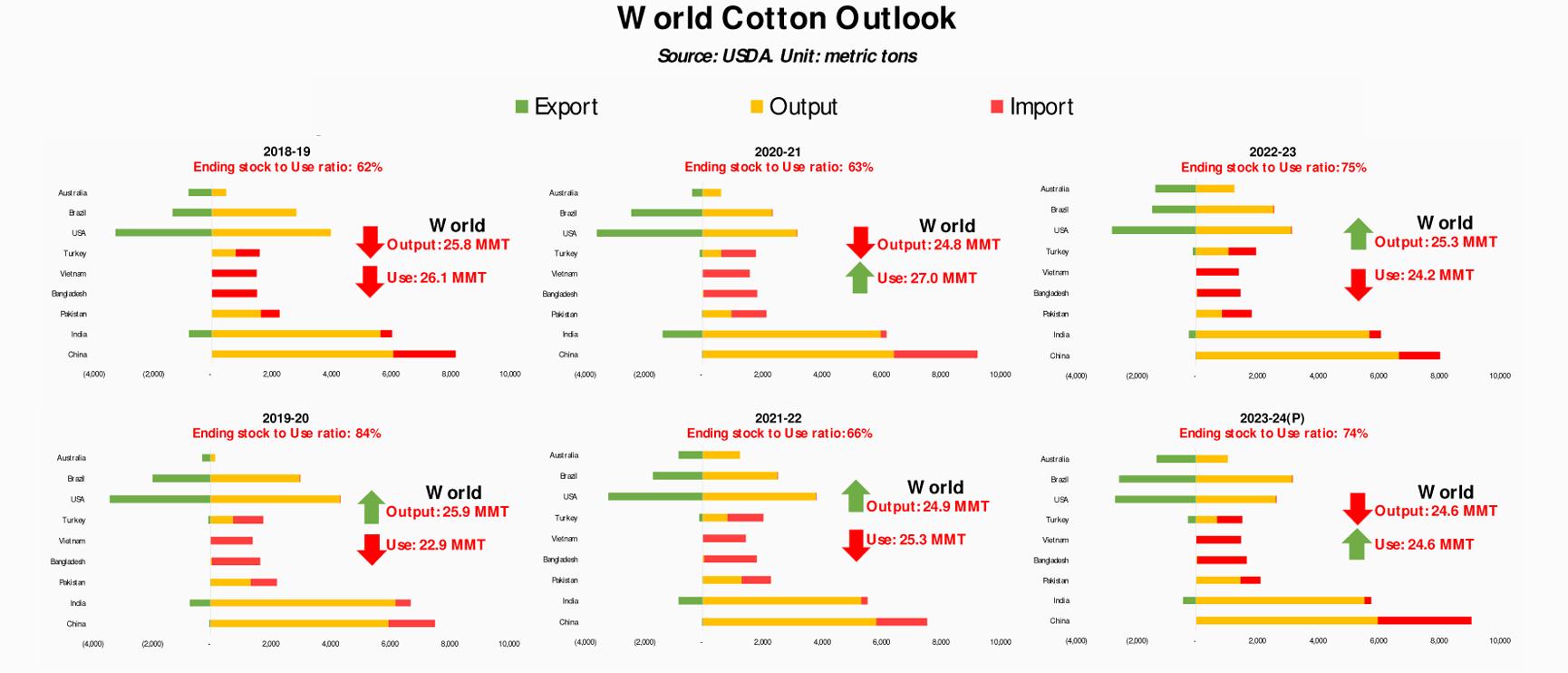

That can only mean terrible things for global cotton demand that has undergone a downward tailspin for the last 28 months. World cotton prices have crashed by at least half over the last 27 months, without so much as recording a nascent recovery in mill consumption across the world.

World consumption is still 3 percent below post-pandemic rally of 2021-22, and only 5 percent higher the pandemic year. At 80 cents per lb, prices are now flirting with the psychological, long-term bottom, and a further slippage could only mean scarier things for most cotton producers. Remember, at 72 percent stock-to-use ratio, global cotton stocks are now at a decade high level (minus the pandemic year).

And things could not have taken a turn for the worse in a more difficult year. Pakistani textile exporters – already battling cost-side pressures on energy tariffs and high finance cost, are now beset with an even drearier outcome in the form of minimum tax regime on income. Although the tax rationalization on export incomes may have long been in waiting, there is much to be said about timing. Yes, in a cutthroat world – only the most efficient shall survive, but maybe a country perpetually facing balance of payment crises should learn to test the patience of its export industries a little less often.

Nevertheless, many still seem hopeful that the political turmoil in Bangladesh may open up fresh opportunities. It is certainly possible, but let’s not count on Bengali brothers sacrificing profit motive for political freedom far too long. And lest we forget, several major exporters from Pakistan have stitching (and other value-add) operations set up in Bangladesh, which means that slower business in the erstwhile East Wing could lead to even slower yarn and fabric from this side of the subcontinent.

All in all, leading indicators point in only one direction: if exports are to be saved in the short run, then its time for SBP to give exporters a break on markup costs, even if re-emerging inflationary pressures mean that correction in exchange rate becomes overdue. Layout forward guidance for a path to lowering financing cost over the remainder fiscal year for private sector, subject to inflation projections being met. Go for it, and go for it now.

Comments