Flying Cement Company Limited (PSX: FLYNG) was incorporated in Pakistan as a public limited company in 1992. The company is engaged in the manufacturing, marketing, and sale of cement.

Pattern of Shareholding

As of June 30, 2024, FLYNG has a total of 694.8 million shares outstanding which are held by 6381 shareholders. The local general public has the majority stake of 49.70 percent in the company followed by the company’s directors, CEO, and their children holding 44.47 percent shares. Foreign general public accounts for 1.45 percent of the outstanding shares of FLYNG. The remaining ownership is distributed among other categories of shareholders.

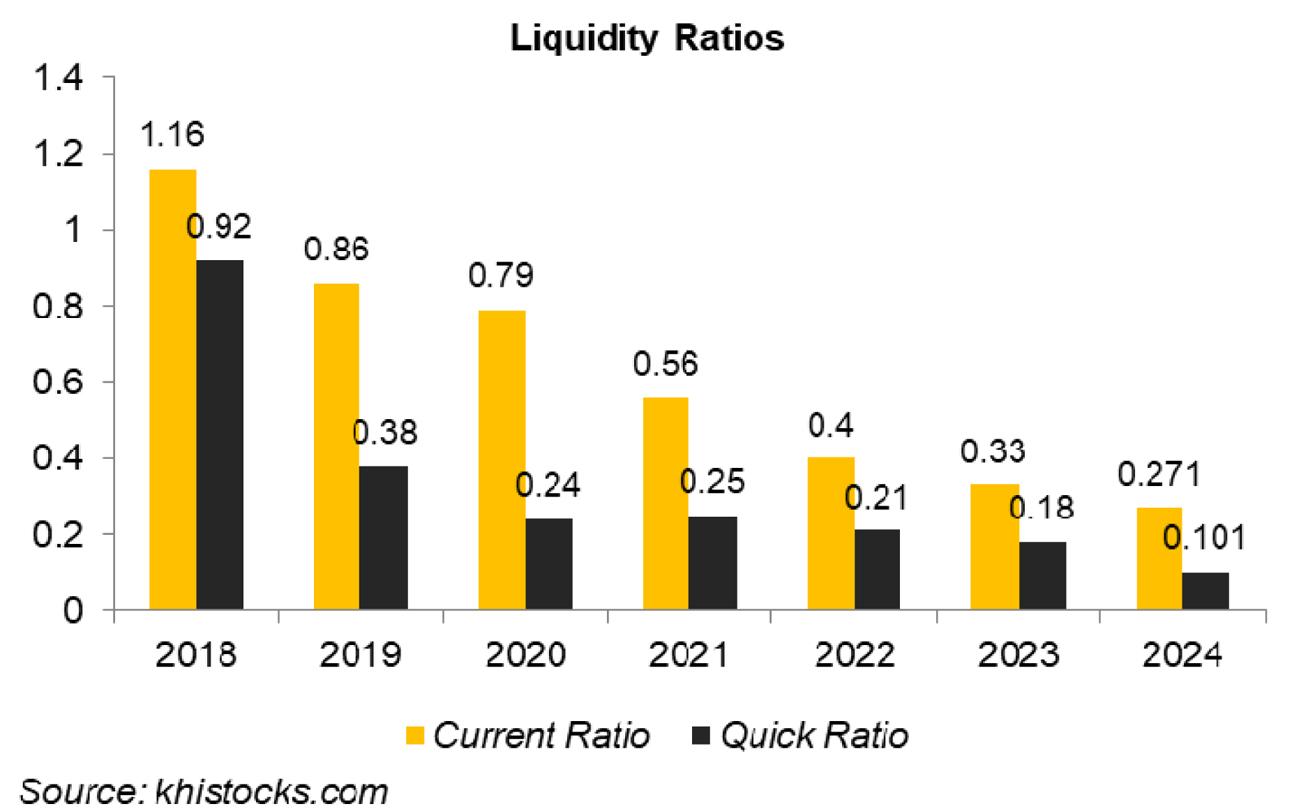

Financial Performance (2019-24)

During the period under consideration, FLYNG’s topline has posted a plunge twice i.e. in 2020 and 2023. Conversely, FLYNG’s bottom line and margins followed a downhill journey until 2020 when the company posted a net loss. In the subsequent two years, the company’s bottom line and margins considerably recovered only to fall again in 2023 and 2024 (see graph of profitability ratios). The detailed performance review of the period under consideration is given below.

In 2019, FYLNG’s topline inched up by 12.40 percent year-on-year. While cement dispatches slid by 2.06 percent year-on-year to clock in at 514,890 metric tons, the topline growth was the effect of upward revision in prices in line with the high cost of production owing to Pak Rupee depreciation, hike in commodity prices, high electricity tariff, inflation as well as the discount rate. Corresponding to reduced off-take, production, and capacity utilization also plummeted in 2019 (see the graph of production and capacity utilization). The cost of sales spiked by 16.10 percent year-on-year in 2019 due to the factors mentioned before. However, it couldn’t be fully passed on to the consumers, resulting in a 25.80 percent dip in gross profit in 2019 with GP margin falling down from 8.83 percent in 2018 to 5.83 percent in 2019. Operating expenses grew by 9.81 percent year-on-year in 2019 mainly on account of higher payroll expenses as the number of employees grew from 347 in 2018 to 398 in 2019. Lower profit-related provisioning resulted in 26.34 percent thinner other expenses in 2019 while other income swelled by 7.34 percent owing to creditors written off during the year. Operating profit slipped by 21.70 percent year-on-year in 2019 with OP margin shrinking from 9.52 percent in 2018 to 6.63 percent in 2019. FLYNG was able to cut back on its finance cost by 25.41 percent in 2019 despite a higher prevailing discount rate. The gearing ratio also narrowed down in 2019 (see the graph of the gearing ratio). Net profit registered a year-on-year decline of 21.57 percent in 2019 to clock in at Rs.142.36 million with EPS falling down from Rs.1.03 in 2018 to Rs.0.81 in 2019. NP margin slid from 6.24 percent in 2018 to 4.35 percent in 2019.

In 2020, FLYNG’s topline posted a drastic 67 percent year-on-year erosion. This was on account of the global recession that kick-started owing to the advent of COVID-19. Cement dispatches posted a steep decline of 83 percent year-on-year to clock in at 86,957 metric tons in 2020. Owing to sluggish demand and the closure of the plant due to lockdown, FLYNG could operate its cement plant at 12 percent capacity in 2020 versus 71 percent capacity utilization recorded in 2019. The clinker plant functioned at 27 percent capacity in 2020 versus 68 percent capacity utilization recorded in 2019. The cost of sales also plummeted, however, with a lower magnitude of 49.95 percent due to inefficient absorption of fixed costs in 2020. FLYNG registered a gross loss of Rs.462.38 million in 2020. Operating expenses mounted by 11.68 percent year-on-year in 2020 due to higher payroll expenses, insurance as well as fee & subscription charges. FLYNG’s workforce further grew to 415 employees in 2020. The company didn’t book any provision for WWF and WPPF in 2020; hence there was no other expense. Other income also marched down by 3 percent in 2020 owing to fewer creditors written off during the year. Operating loss clocked in at Rs.432.86 million in 2020. Finance costs magnified by 144.40 percent in 2020 due to higher discount rates for most part of the year coupled with excessive borrowing which drove up its gearing ratio to 47.3 percent in 2020. FLYNG recorded a net loss of Rs.530.72 million in 2020 with a loss per share of Rs.3.02.

In 2021, FLYNG’s topline posted a staggering year-on-year rise of 196.96 percent. This was on account of continued efforts put in place by the government to boost the real-estate sector; the revival of CPEC activities as well a low discount rate which encouraged investors to park their savings in the sector. FLYNG’s dispatches grew by a robust 346 percent growth to clock in at 388,157 metric tons in 2021. Capacity utilization also jumped up to 55 percent and 43 percent for cement and clinker plants respectively in 2021. Cost of sales grew by 88.26 percent year-on-year in 2021. The company posted a gross profit of Rs.302.94 million in 2021. GP margin also considerably recovered to clock in at 9.45 percent as the company also increased its prices during the year due to demand recovery. FLYNG was able to trim down its operating expenses by 2 percent in 2021 by cutting down its legal & professional charges, communication charges as well as fee & subscription charges. The contraction of these charges offset the higher payroll expenses incurred during the year as FLYNG’s workforce rose to 544 employees in 2021. Higher sales of trees, scrap, and damaged stock pushed other income up by 10.88 percent in 2021. FLYNG posted an operating profit of Rs.325.37 million in 2021 with OP margin clocking in at 10.15 percent. Finance costs slid by 10.36 percent in 2021 on account of the low discount rate. The company posted a net profit of Rs.143.68 million in 2021 with EPS of Rs.0.38 and an NP margin of 4.48 percent.

The ascending journey of FLYNG’s net sales continued in 2022 with a 66.46 percent year-on-year rebound in net sales. This came on the back of a 35 percent rise in its off-take which clocked in at 522,881 metric tons in 2022. Economic activities continued to pick up post-COVID-19 buttressing the construction and real-estate sector. In line with the rising demand, FLYNG operated its cement and clinker plant at 63 percent and 76 percent capacity respectively. While there was an upsurge in demand in 2022, there were grave downside risks to the company’s performance which included political headwinds, the Russia-Ukraine crisis, sharp appreciation of electricity tariff, elevated fuel & energy prices as well Pak Rupee depreciation. Yet, FLYNG was able to significantly drive up its GP margin to 16.34 percent in 2022 by raising its prices and also by adopting of Waste Heat Recovery Power Plant which rendered significant cost savings in power consumption. Operating expenses escalated by 40 percent year-on-year in 2022 due to higher payroll expenses, utility charges, fee & subscription charges as well as donations. Higher profit-related provisioning pushed up other expenses by 125.86 percent in 2022; however, no creditors written back during the year resulted in 17.62 percent less other income earned during the year. Operating profit magnified by 153.96 percent in 2022 with OP margin climbing up to 15.5 percent. Finance cost surged by 60.58 percent in 2022 on account of the high discount rate although there was a slump in external borrowings during the year. Net profit magnified by 544.54 percent year-on-year in 2022 to clock in at Rs.926.10 million with EPS of Rs.1.33 and NP margin of 17.36 percent.

FLYNG’s net sales succumbed to geopolitical, economic, and political uncertainties and tumbled by 20.48 percent year-on-year in 2023. Destructive floods in 1QFY23 also halted the construction and infrastructure-related activities in the southern region of the country, impeding the cement demand. FLYNG’s dispatches dwindled by 37 percent year-on-year in 2023 to clock in at 329,211 metric tons. Capacity utilization also shrank to 42 percent and 47 percent for cement and clinker plants respectively in 2023. Constant currency depreciation, high inflation as well as hike in energy tariff didn’t allow FLYNG’s cost of sales to slide down by the same magnitude as its net sales, resulting in 33.84 percent leaner gross profit and GP margin slipping down to 13.6 percent in 2023. Operating expenses spiked by 15.98 percent year-on-year in 2023 on account of a considerable rise in payroll expenses, directors’ remuneration, advertisement, and communication expenses incurred during the year. Other expenses dived down by 39.93 percent in 2023 owing to lesser provisioning for WWF and WPPF. Other income ticked up by 5.18 percent in 2023 on account of higher sales of trees, scraps, and damaged stock. Operating profit narrowed down by 34.86 percent year-on-year in 2023 with OP margin plunging to 12.68 percent. Finance costs swelled by 46.40 percent year-on-year in 2023 due to monetary tightening and increased borrowings. As a consequence, net profit weakened by 70.71 percent year-on-year in 2023 to clock in at Rs.271.25 million with EPS of Rs.0.39 and NP margin of 6.4 percent.

Shrinking pockets of consumers, exorbitant cement prices, mounting discount rates, and wavering investor confidence due to political uncertainty resulted in a marginal 6.44 percent year-on-year growth in FLYNG’s net sales in 2024. Cement dispatches went down by 4.36 percent to clock in at 314,854 M tons. This shows that the topline growth was merely the result of a price hike. The cost of sales mounted by 14.20 percent in 2024 due to heightened energy tariffs and inflationary pressure. This resulted in a 42.90 percent contraction recorded in FLYNG’s gross profit in 2024 with GP margin drastically falling down to 7.29 percent. Operating expenses surged by 15.97 percent in 2024, particularly on account of payroll expenses as well as directors’ remuneration. The company expanded its workforce from 540 employees in 2023 to 553 employees in 2024. Other expenses dipped by 3.49 percent in 2024 due to lower profit-related provisioning done during the year. Higher sales of trees, scrap, and damaged stock as well as agricultural products drove other income up by 259 percent in 2024. Operating profit eroded by 4.8 percent in 2024 with OP margin marching down to 11.35 percent. Finance costs escalated by 6 percent in 2024 due to a higher discount rate. This was despite the fact that the company settled a considerable portion of its outstanding long-term liabilities during the year. This drove down its gearing ratio from 30.24 percent in 2023 to 28.68 percent in 2024. FLYNG recorded a net profit of Rs.51.45 million in 2024, down 81 percent year-on-year. This translated into EPS of Rs.0.07 and NP margin of 1.14 percent.

Recent Performance (1QFY25)

With the phased recovery in economic indicators such as declining inflation, stable Pak Rupee, monetary easing, and encouraging foreign exchange reserves, cement demand which had been biting the dust for the past two years began to recover. FLYNG recorded 34.93 percent growth in its net sales in 1QFY25. However, heightened fuel and power costs didn’t allow the company to record any improvement in its gross profit during the period which fell down by 61.4 percent in 1QFY25. The company couldn’t pass on the impact of cost hikes to its consumers due to frail demand. This resulted in the GP margin falling down from 20.91 percent in 1QFY24 to 5.98 percent in 1QFY25. Operating profit grew by 5.6 percent in 1QFY25 due to higher freight charges and utility expenses. Operating profit plummeted by 70 percent in 1QFY25 with OP margin clocking in at 4.11 percent versus OP margin of 18.52 percent recorded during the same period last year. Monetary easing as well as settlement of outstanding liabilities resulted in a 61.40 percent decline in finance cost in 1QFY25. Net profit narrowed down by 73.55 percent to clock in at Rs.23.5 million in 1QFY25. This culminated in EPS of Rs.0.03 versus EPS of Rs.0.13 recorded during the same period last year. NP margin also fell from 7.75 percent in 1QFY24 to 1.52 percent in 1QFY25.

Future Outlook

The corrective measures taken by the authorities have resulted in an uptick in the value of local currency off-late. This coupled with ease in inflationary pressure, reversal of the monetary cycle, and increased investor confidence will positively impact the cement industry. Higher PSDP spending in the second half of FY25 will also support the industry volumes. However, amid subdued demand and high costs, cement manufacturers will struggle for margin growth.

office")

Comments