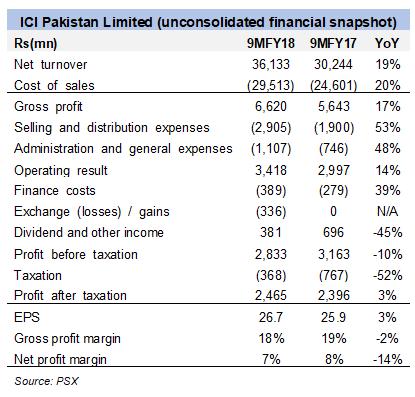

ICI continued its double digit growth path for the current financial year with higher revenue across all business divisions except chemicals & agri science business. Robust growth in divisions of polyester, soda ash, and life sciences businesses helped drive the increase in operating result. Life sciences led the growth with a 36 percent increase in sales followed by polyester that grew by 23 percent year-on-year for 9MFY18.

Polyester is the biggest business segment of ICI which is why the 122 percent increase in operating result in 9MFY18 drove ICI’s overall profitability. PSF margins have had a somewhat rollercoaster ride in 3QFY18. The start of the year saw a decline in international PSF margins as the prices of its key ingredients MEG and PTA rose; MEG prices were at their highest level since December 2013 in January, while PSF prices saw a downward dip.

This trend continued in February but reversed in March when PSF margins increased nearly by 12 percent month-on-month. MEG prices declined to offset the continued increase in PTA prices, while PSF’s prices recovered to their previous level.

However, market for PSF has been growing with increased demand generated by the textile sector, improved power availability and anti-dumping protection on PSF. As a result, overall the period saw increase in PSF sales as well as margins.

Life sciences’ operating result for 9MFY18 rose by 48 percent due to double digit growth in its pharmaceuticals and animal health divisions. It appears that ICI’s acquisition of Cirin Pharmaceuticals (Pvt.) Limited enhanced its manufacturing capabilities and sales network, as well as diversified its product portfolio as intended.

Other investments in its pharma division last year include ICI’s partnership with Ferrer and Smith & Nephew and the acquisition of some key brands and assets of Wyeth Pakistan Limited.

Increase in profitability of the life sciences and polyester division compensated for the chemicals and agri sciences business, which has been suffering due to the severe liquidity crunch in the agricultural sector. The recording of provision of bad debts against receivables impacted this segment’s profits and brought down the company’s overall profitability despite chemicals & agri business being the smallest division of ICI.

Higher exchange losses because of the devaluation of rupee and lower dividend income from associates drove down profit before tax. Since ICI uses a coal mix ratio of 70:30 for imported and local coal respectively for soda ash, and the polyester plant uses imported coal entirely, devaluation of the rupee adversely impacts ICI’s fuel costs.

However, the devaluation impact on soda ash seems limited as ICI expanded its soda ash production plant capacity by 75,000 tons per annum in the last quarter. The total installed capacity currently stands at 425,000 tons through which it caters to about 70 percent of the local market.

Comments

Comments are closed.