Oil marketing companies have seen a significant change in their revenue mix in the last three to four years. Where rising furnace oil volumes were seen shrinking, retail fuels like diesel and petrol took the centre stage along with LNG. Pakistan State Oil Company Limited (PSX: PSO), the largest OMC has also seen a shrink in its black oil market while volumes have increased in the white oil market. However, recently due to the rise in competition and increased prices, lower demand and depreciating currency, the boom in petroleum sales even for retail fuels has hit a snag.

PSO is engaged in marketing and distribution of all forms of POL products including Motor Gasoline (Mogas), High Speed Diesel (HSD), Furnace Oil (FO), Jet Fuel (JP-1), Kerosene, CNG, LPG, Petrochemicals and Lubricants. It also imports products based on the demand. These include Mogas, HSD, JP 1 and FO as and when required.

With 3,514 outlets across Pakistan, PSO has the largest distribution network through which it serves both retail and bulk customers. More than half of this retail and over 160 consumer business outlets have been upgraded with the state-of-the-art modern-day facilities in accordance with the company's New Vision Retail Initiative. With 9 installations and 23 depots located across the country, PSO's storage capacity is the largest in the country and is approximately a million metric tons, representing 68 percent of the total storage capacity owned by all the OMCs.

Pattern of shareholding and share price PSO's shareholding is divided such that the Government of Pakistan holds around 22.47 percent; NBP Trustee Department has 14.88 percent shareholding. A breakup of the shareholding at PSO is shown in the illustration

The firm has strategic investments including 12 percent in Parco's White Oil Pipeline Project; 22.5 percent in PRL; 22 percent in Pak Grease Manufacturing Company Limited; 49 percent in Asia Petroleum Limited; and 62 percent investment in Joint Installation of Marketing Companies, and 50 percent in new Islamabad airport fuel farm.

Financial performance FY17 FY17 was the year where PSO took the lead and became the first OMC to introduce the higher grade RON environment-friendly gasoline brands Altron Premium and Altron X High Performance. FY17 was a year retail fuels, PSO also introduced Action+ Diesel, a superior quality and environment friendly Euro-II compliant diesel.

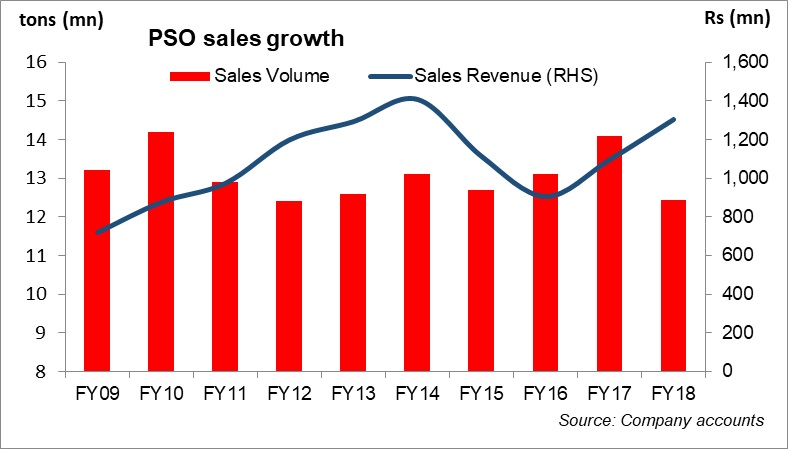

Resultantly, sales volumes for the firm increased by 8 percent year compared to a growth ranging between -9 percent to 4 percent in the previous six fiscal years. Rise in volumes along with higher prices and also the RLNG business led to 30 percent year-on-year surge in the firm's revenue.

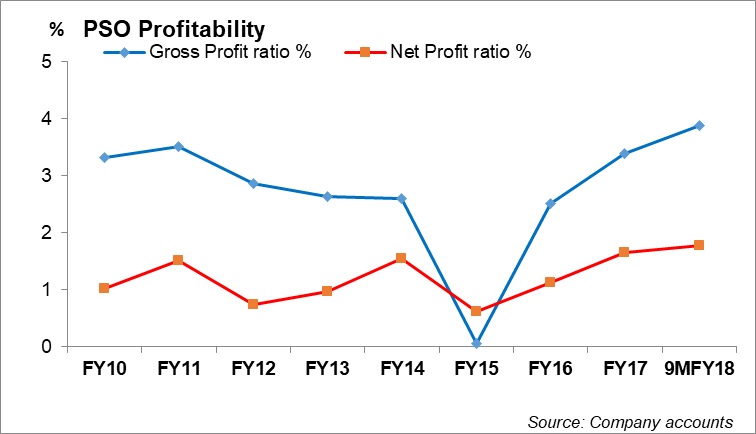

Amid changing oil dynamics and market share, PSO continued to lead the market with overall 54.8 percent market share. Market share of black oil that comprises of furnace oil rose to 73 percent from 70.5 percent in FY16 where PSO achieved 12.5 percent increase in FO sales to the power sector on a year-on-year basis, whereas the market share in white oil (Mogas, HSD, SKO, Jet Fuel) stood at 43.9 percent versus 46.8 percent. Its LNG business continued with 58 LNG vessels supplied during the year carrying 186,672,980 MMBTU. Rise in PSO's net revenues led to 77 percent increase in its bottom line for FY17. Other factor that lifted the bottom line was the reduction in the finance cost.

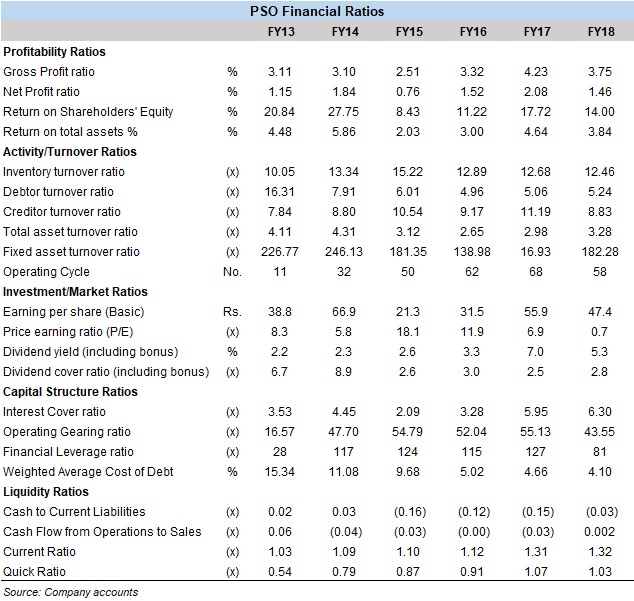

However, the company's liquidity position remained weak. As cash to current liabilities deteriorated by 25 percent for PSO mainly due to increase in current liabilities on account of higher short term borrowings. The firm's inventory turnover ratio decreased by 7 percent in FY17 due to increase in stock in trade by 30 percent, which was partly offset by increase in sales by 21 percent.

FY18 performance PSO's market share in FY18 in overall oil market was around 50 percent, and it witnessed growth in the white oil segment, especially motor spirit and HSD. In FY18, it witnessed strong growth of 10.1 percent in MOGAS, 2.4 percent in HSD and 9.1 percent in JP-1 sales volumes. Retail sector however, faced stiff competition from new entrants, substantial discounts offered by competitors and the influx of smuggled products like diesel from Iran.

However, its black oil segment saw a significant slide owing to the supply situation and availability of RLNG and the government's strategy of switching priority (merit order) of existing power plants to RLNG/natural gas. PSO's FO sales volume declined by 29.6 percent year-on-year in FY18. The lubricants business recorded an increase of 4.4 percent year-on-year in the fiscal year.

In FY18. PSO's gross revenues increased by 19 percent, year-on-year, while profit after tax went down by 15.2 percent year-on-year primarily on account of one-time reversal of deferred tax asset; decrease in other income by 32.7 percent as PIBs matured in July 2017 resulting in lower interest income; and increase in other expenses by over 40 percent due to higher exchange losses on account of significant currency depreciation. However, increase in gross profits despite major decline in furnace oil sales occurred mainly because of increase in margins of petrol and jet fuel along with higher margins were FO and LNG due to higher international prices. Bottom line decrease was also reduced somewhat because of a decline in finance cost inFY18.

On the liquidity side, the company's cash to current liabilities improved in FY18 primarily due to decline in short term borrowings by 31.2 percent. Its inventory turnover decreased in FY18 because of increase in inventory due to increase in international oil prices.

1HFY19 and beyond

The volumetric growth outlook for petroleum products is not robust for FY19. The sector has been witnessing consolidating retail volumes for some time along with staggering decline in FO. 1HFY19 depicted a slide of around 50 percent year-on-year in PSO's earnings, and the company's revenues growth remained tepid. Some respite to revenues came from lubricant and LPG sales.

PSO's market share in 7MFY19 stood at 40 percent in the overall liquid fuel segment versus 54 percent in 7MFY18. This was not only led by declining furnace oil market share from 73 percent to 45 percent, but also a decline in motor gasoline and diesel market shares; down from 41 percent to 36 percent, and 46 percent to 38 percent, respectively.

The company's decline in earnings for the period came from higher exchange losses and inventory losses. Inventory loss came from high inventory of FO, which could not be sold due to low power demand while the same led to refineries lowering their selling prices, which further exacerbated the squeezing effect on earnings. The firm's net profit came down by over 50 percent, year-on-year in1HFY19, and besides weak volumes and inventory losses, PSO's decline in other income (penal income) and staggeringly high finance cost in the period were the key factors behind the dismal performance.

Other headwinds for the sector are omnipresent circular debt. PSO continues to face liquidity issues due to the circular debt and the resultant power sector receivables. However, the firm is hopeful of the possibility of Rs200 billion circular debt clearance attempt by the government

===================================================

PSO-Pattern of Shareholding as at June 30, 2018

===================================================

Categories of Shareholders' %

===================================================

Members-Board of Management, Chief Executive 0.01

Officer and their spouse and minor children

Associated Companies, Undertakings

and related parties

Government of Pakistan 22.47

GOP's Indirect Holding:-PSOCL 3.04

Employee Empowerment Trust

NIT and ICP 0.09

Banks, Development Financial Institutions, 5.28

Non-Banking Financial Institutions

Insurance Companies 9.33

Modarabas and Mutual Funds 15.62

Shareholders holding 10% or more:

NBP, Trustee Department 14.88

General Public:

Resident 14.27

Non-resident 0.39

Others:

Non-Resident Companies 6.85

Public Sector Companies & 6.67

Corporations and Joint Stock Companies

Employee Trusts/Funds etc. 1.1

100

===================================================

Source: Company accounts

Comments

Comments are closed.