Gharibwal Cement (PSX: GWCL) is a cement manufacturer located in district Chakwal of Punjab supplying to northern domestic markets in Pakistan. Incorporated in 1961, the company started its operations in 1965 with an annual capacity of 360,000 tons. A decade later, it was nationalised and in 1993 denationalised along with many of its peers. The company expanded operations over the years. In 2003, it merged with GCL Electric with a power generation capacity of 10MW in 2003, later adding on two gas power generators of 12 MW. In 2009, a new plant was added with more than 2 million tons annual capacity that came with three dual-fuel power generators of 16MW. In 2011, the company discarded its old plant that had an annual capacity of 540,000 tons and was left with the 2 million tons of capacity which it is currently using. In 2013, Gharibwal upgraded its electric grid stations and recently, the company invested in a 20 MW of a Waste Heat Recovery (WHR) unit and a downhill conveyor belt to improve the operational performance of its plant. Based on 2 million tons of production capacity, the company used to have 5 percent in the market overall, but since new expansions have come in; the company's share in market capacity has fallen to 4 percent.

Shareholders and investments

The company's shares are pretty concentrated toward a major category of directors and family members as nearly 89 percent of the company's shares are held by them, of which the CEO held more than 56 percent of the shares as on June 2018. The rest of the shares spread across joint stock companies, banks and modrabas and foreign companies with the public holding just 6.2 percent shares.

======================================================== Pattern of Shareholding (as on June 30, 2018) ======================================================== Categories of Shareholders Share ======================================================== Directors and their spouse(s) and minor children 88.8% Mr. Abdur Rafique Khan 22.7% Mr. Muhammad Tousif Peracha- CEO 56.3% Mr. Nazir Ahmed Peracha 0% Mr. Muhammad Niaz Peracha 0% Mr. Ali Rashid Khan 4.0% Mr. Daniyal Jawaid Parcha 0.0% Mrs. Tabassum Tousif Peracha 0.1% Mrs. Amna Khan 5.7% Mrs. Salma Khan W/O A. Rafique Khan 0.0% Modarabas and Mutual Funds 0.02% Joint Stock Companies 0.37% Foreign Companies 2.9% Associations 0.01% Others 0.2% Banks, development finance institutions, 1.49% non-banking finance companies etc. General Public 6.2% Total 100% ========================================================

Source: Company accounts

In the past two years, Gharibwal has upgraded its facilities and completed two BMR projects. To cut down on power costs, it installed a waste heat recovery plant as well as. Other investments include a downhill conveyor belt, a new vertical cement mill which optimises the grinding capacity as well as a clinker storage silo to enhance clinker storage and reduce the handling and transportation cost of clinker stock.

Gharibwal has also been providing loans to its associate company Balochistan Glass Limited (BGL). BGL has three glass plants, located in Hub-Balochistan, and Lahore Sheikhupura road. BGL is selling its tableware products under the brand name of "Marimax" in addition to manufacturing glass containers, and plastic shells for beverage companies. In 2018, the board of directors of Gharibwal approved a facility of Rs500 million including Rs350 million as short term loan and advance and a letter of credit facility for procurement of inputs and working capital needs. Gharibwal earns a mark-up of 1 percent above the rate charged by banks and financial institutions for this loan.

Operational and financial performance

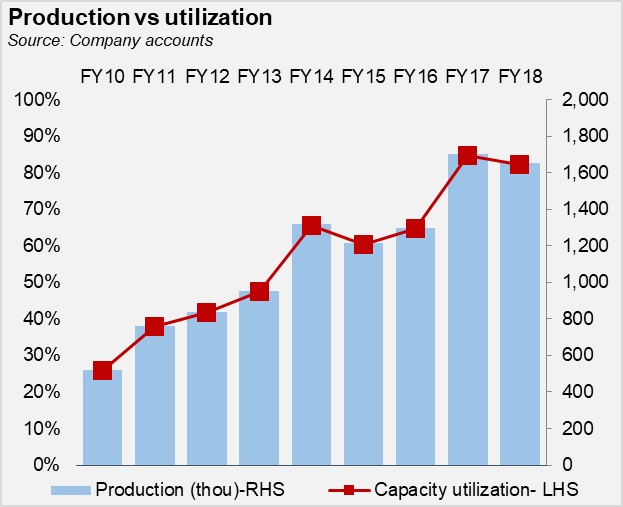

Between FY10 and FY18, Gharibwal cement has raised production by three times. The capacity utilization was really low in the beginning years-in FY10, it was 26 percent but after it discarded its old plant in 2011, the company raised capacity utilization significantly with the new plant. By FY14, it was 66 percent, and 85 percent by FY17. The local demand had also blossomed during these years, and growing retention prices in the domestic market also allowed the company to keep growing its revenues. Since FY10, the revenues have grown by 5 times. At Rs11 billion in revenues, not so gharib after all!

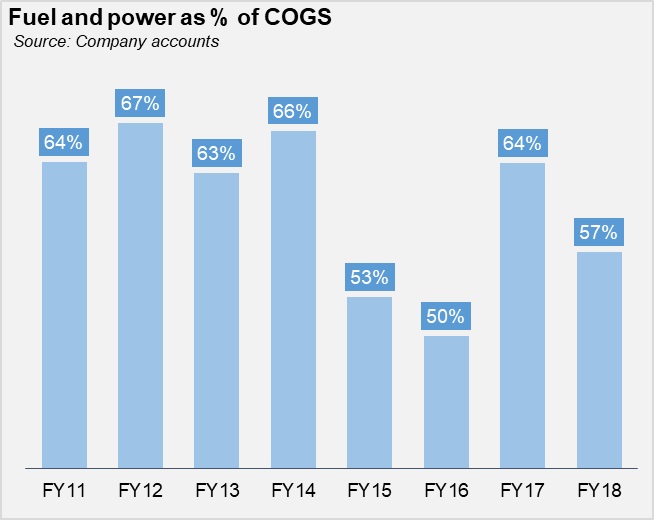

Though in FY18, the company produced some units less than the previous year; the revenues slightly grew as the company fetched better prices even though there were fluctuations in major northern markets. Margins depend on demand, prices that the sold units fetch and direct costs. Though the company has grown its margins from a gross loss of 20 percent during FY10 to 40 percent during FY16, the past two years have been tougher on Gharibwal and the rest of the industry. Coal and other imported fuel make up for majority of the costs for the cement manufacturers. With the Balancing, Modernization and Replacement (BMR) conducted by the company, Gharibwal managed to reduce fuel and power costs as share of cost of sales from 64 percent in FY11 to 50 percent in FY16. However, rising coal prices in the international markets and depreciation of rupee during FY18 brought these costs back up to 64 percent in FY17 and down to 57 percent in FY18.

According to the company's annual report, the cost per clinker rose by 22 percent during FY18 due to international coal prices while prices were also higher for gas, furnace oil and grid electricity. Imported fuels also get impacted by the depreciating rupee in that it becomes expensive. The company claims it mitigated the effect of these price hikes by generating 43 percent of the total electricity at significantly lower costs against 10 percent during FY17. As per the annual report: "The increased use of the waste heat recovery system helped in limiting the power and fuel cost (which constituted approximately 57% of the total manufacturing expenses) increase to just 6% over the previous year, otherwise, this impact would have been significantly higher".

The margins fell down from 40 percent in FY16 to 34 percent and 24 percent in FY17 and FY18. Lower gross profits put pressure on the net profits-profit margins fell from 26 percent to 20 percent to 13 percent between FY16 and FY18.

Latest financials and outlook

As the cement industry entered the FY19, times have dramatically changed. With the Nawaz government out, the expansion of the economy was also out. The new government is busy with stabilisation efforts to control the twin deficits, for which it is also seeking an IMF bailout. Construction activities depend highly on infrastructure developed undertaken by the government in its mega development projects. With PSDP cuts, policies to curb grey money pouring into the real estate sector (restriction on non-filers to purchase property of over Rs4 million), and overall economic downturn, cement demand in the market has reduced substantially-particularly in the north zone.

Companies have had to rely more on exports but even there, the north players have hit a snag-Indian market has all but shut down trade with Pakistan through 200 percent tariffs on Pakistani goods, while Afghan market is become ever so difficult to penetrate as it has opened its doors to other cement exporters. Cement companies in the south have been selling overseas (a good share of which is low-priced clinker), given their proximity to the seaport. They have managed to keep growth in the local as well as exporting markets. Gharibwal has witnessed a drop of 17 percent in dispatches in 9MFY19, which translated to 3 percent decline in revenue-not too bad!

The company clearly has fetched better prices in the domestic market for its cement in nine months (revenue per ton rose by a whopping 17 percent which is very impressive). However, net profits fell by 18 percent as gross profits depleted (company's costs per ton rose by 18 percent); indirect expenses rose by 2 percent (5 percent of revenues) and finance costs also grew which is a substantial amount (4 percent of the revenues). The higher costs of course have to do with the dual effect of higher average coal prices during the 9M period and the depreciating rupee that has wreaked havoc.

In the upcoming months, since demand is not expected to see a major U-turn, cement companies will be trying to manage their cash flows and inventories effectively. They are still profitable but the slope can be slippery.

======================================================= Gharibwal Cement (Financial performance in 9M) ======================================================= Rs (mn) 9MFY19 9MFY18 YoY ======================================================= Sales 8,276 8,513 -3% Cost of Sales 6,355 6,451 -1% Gross Profit 1,921 2,061 -7% Administrative 282 280 1% Distribution costs 23.5 14.0 67% Other operating expenses 86.3 101.7 -15% Finance income 26.9 19.9 35% Finance cost 356.4 298.7 19% Profit before tax 1,200 1,387 -13% Taxation 380 386 -2% Net profit for the period 820 1,000 -18% Earnings per share (Rs) 2.05 2.5 -18% Dispatches (tons) 1,187,949 1,428,071 -17% GP margin 23% 24% -4% NP margin 10% 12% -16% =======================================================

Source: PSX notice

bill likely to be challenged in courts’")

Bill, 2024: comments")

Comments

Comments are closed.