Among major autoparts manufacturers, Loads Limited (PSX: LOADS) is a prominent name. Established in 1979, the company started commercial production in 1985. The company manufacturers exhaust systems, mufflers, radiators and sheet metal components for the domestic automotive industry, though it does want to export. The major business for Loads come from exhaust systems which take up 60 percent or more of the business while radiators take 20 percent and the rest is sheet metal components.

The company supplies autoparts to all the three major car assemblers, while also catering to commercial vehicles and tractors. The company has three plants located in Korangi and Bin Qasim. It has been manufacturing parts in collaboration with major Japanese autoparts makers including Futuba, Toyo Radiator, Sankei Giken and SNIC.

Loads is part of the Ali group with several other major listed companies such as Packages Limited (PSX: PKGS), IGI Insurance Limited (PSX: IGIIL), and Treet Corporation Limited (PSX: Treet) within it. Loads has four fully owned subsidiaries: Specialized Motorcycles, Specialized Autoparts Industries, Multiple Autoparts Industries and High-tech Autoparts.

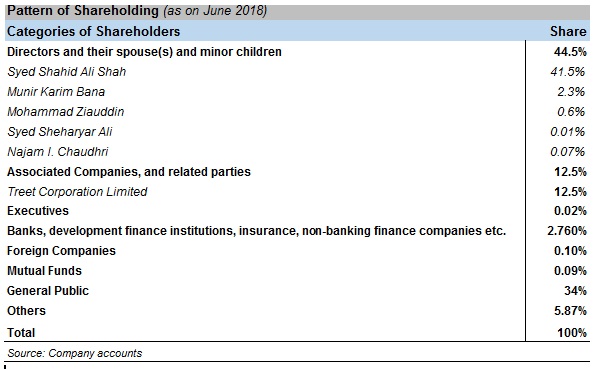

The High-tech Autoparts subsidiary is manufacturing Aluminium Alloy Wheels, which are typically now being used in high end models, and involved a hefty investment from Loads. The company went through an Initial Public Offering (IPO) in 2016 having raised Rs 1.7 billion. The company was sponsored by Treet Corporation, which held 20 percent shares in the company. The associated company held 12.5 percent shares in June-18 with voting rights. The Chairman of Loads, Syed Shahid Ali Shah held 41.5 percent of the company's total shares while its CEO, Munir Bana held 2.3 percent of the shares in FY18. The general public held 34 percent of shares.

Recent Financial and Operational Performance

The company's topline represents marked improvement in the business following a trajectory close to the performance of the automobile industry. Though like auto assemblers, Loads is also sensitive to commodity prices in the global market as well as the dollar-rupee parity since it imports its inputs from abroad. Other cost factors such as electricity and gas prices which are themselves dictated by fuel prices abroad also affect how Loads margins fare. With a growing revenue stream, the company has seen its margins shrink since 2015, coming to 11-12 percent in FY17 and FY18, from 15-16 percent in the preceding years.

Though during FY17, the company's margins primarily dropped due to the depreciating cost on the capitalization of plant and equipment. On the profit margins front, in FY15 they stood at 6 percent, coming down to 4 percent in FY16 but back up to 7 percent in FY17. This improvement came due to savings in finance charges such as tax credits on listing and capital expenditure. This led to the 70 percent growth in the bottom line of the company that year. However, profits subsequently dropped in FY18 despite high sales volumes and revenues due to the rising cost scenario that took over the economy during that year.

Outlook

The company's sales are pegged to automobile volumes. In FY18 for instance, sales for exhaust system grew because of new models of Honda Civic and Suzuki but were offset by Toyota Corolla volumes as well as falling bus sales. The phasing out of Suzuki Mehran does not bode well for many automakers. For Loads, it means lower sales for radiators since Alto will be using imported aluminium radiators. And with the way things are headed, the company is close to incurring a loss in FY19, even as the excitement of new entrants hangs in the air.

In 9MFY19, the company net margins have dropped to 1 percent-from 6 percent despite a healthy growth of 30 percent to revenues and only a slight decline in gross margins to 12 percent-from 13 percent in 9MFY18. The company revenues remained strong (sales for exhaust systems for instance grew by 49 percent) even as tractor and truck volumes have critically decline during the nine months. Car sales have remained robust and it's important to note that cars, which are more localized have seen a positive growth in the overall industry. Both Toyota and Suzuki cars have grown during FY19, and upward price adjustments may also have helped shore revenues for Load.

Meanwhile the depreciating rupee may have hurt Loads margins, but not by a lot. The real kicker comes in when looking at finance costs which have tripled in nine months against 9MFY18. They are now 4 percent of net revenues against 2 percent the previous year. This borrowing cost may further go up as interest rates climb. The company also paid dramatically higher taxes in 9MFY19 due to minimum turnover tax.

In its annual report for FY18, the company claimed that it would continue with its "aggressive plans to invest in expansion and modernization to capitalize on the benefits of new entrants". However, the current financial standing of the company is not conducive to more expansions as it tries to survive the existing economic downtime. New players entering the auto sector is positive for Loads but localization will probably not start immediately for these players. It comes down to Loads and how actively it pursues these new ventures.

It is clear that in FY19, automotive sales have dropped, not only for commercial vehicles, but also for cars and this trend will continue on during FY20 and may even worsen for players like Suzuki that are still breathing above water. One thing is for sure, if autoparts manufacturers had lent focus on regional markets outside of Pakistan, they could have survived this slowdown far better.

Comments

Comments are closed.