Located in Hub, Balochistan, Attock Cement (PSX: ACPL) is one of a mid-range manufacturers of cement with operations established in 1981 and commercial production starting in 1988 with a capacity of 0.6 million tons per annum. Attock's cement is popularly known by its brand name Falcon, which is supplied mainly to the southern parts of the country as well as abroad through the sea port. Main exporting markets include Sri Lanka, Mauritius, Sudan, India, Tanzania and Somalia. Through a series of expansions, with the latest line added in FY18, the company boasts a production capacity of 3 million tons. Its market share in the south is around 25 percent or more. The company was started with an initial capital outlay of Rs1.5 billion and a foreign exchange component of $45 million. The company is currently running three manufacturing plants at its facilities.

Attock also made investments in a cement grinding unit in Iraq through a joint venture with the Iraq-based Al Geetan Commercial Agencies to form a subsidiary, a limited liability company. Attock's holds 60 percent of the company. The mill has a capacity of 0.9 million tons at a cost of $24 million.

ACPL is part of the Pharaon group has a range of investments in the areas of oil and gas, power generation and information technology. Aside from Attock cement, the group also includes Pakistan Oilfields Limited (1950), Attock Refinery (1922), Attock Petroleum Limited jointly established by the Pharaon Investment Group Limited Holding (PIGL) and Attock Oil Group of Companies (1995). Pharaon also took over National Refinery Limited (NRL) in 2005.

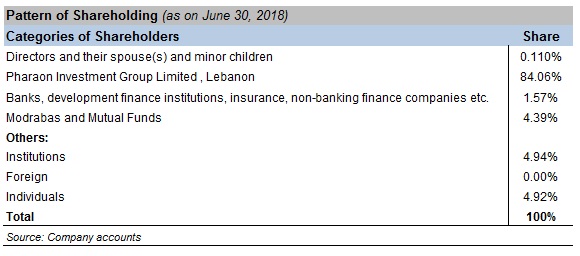

In terms of shareholding, Pharaon Investment, which is the holding company of ACPL held more than 84 percent shares in the company in June 2018 (FY19 annual report is not out yet). The rest of Attock's shares are distributed between banks, DFIs, Modrabas, Mutual Funds and institutional investors. The public held 4.92 percent of the company's shares in that fiscal year.

Operational and financial performance

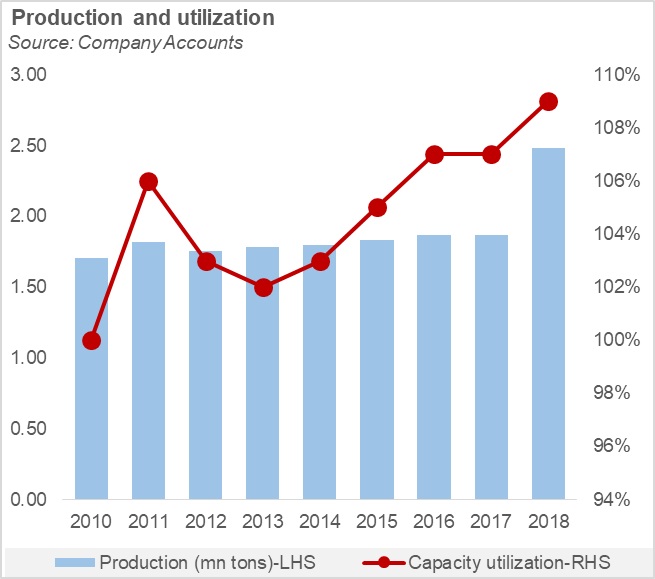

Attock has significant market share in the south and faces limited competition. It has been operating at maximum capacity for a number of years now and its brand recognition ensures it a solid space in the market. The company enjoys proximity to the port which in periods when domestic demand declines can help in shifting focus towards exports. Its cost compared to many cement manufacturers in the north are also lower as it can get its imported raw material and fuels at lower freight.

The south zone enjoys higher cement retention prices because of regional dynamics. Lower competition in the region allows cement manufacturers to charge higher prices. During times of lower domestic demand, the company was able to favor its sales mix toward exports. The company's margins not only depend on off take and prices (which have moved upwards) but also the cost of imports and the exchange rate. International coal prices can also hit the company's margins when they moved upwards while a depreciating rupee makes these imports expensive.

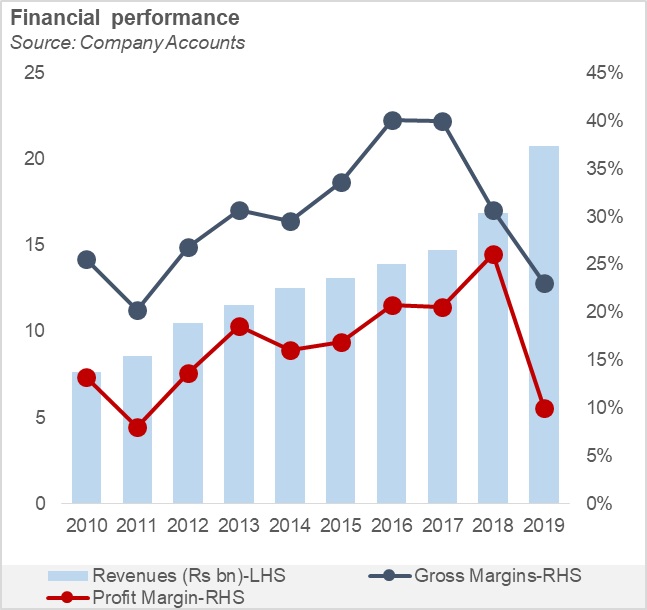

During FY18, for instance, rupee's depleting value against the dollar raised costs and significantly affected margins. Attock's margins that had strengthened previously during FY15 and FY16 (at 40%) on the back of high demand and stable costs, dropped to 31 percent during FY18.

Since the introduction of line-3, the company has been exploring markets such as Bangladesh, Kenya, Tanzania, and Sri Lanka for the export of clinker, according to its official report. Attock's exports share in its sales during FY16- FY18 came down from 39 percent to 19 percent because of fast growing domestic owing to a growth in real estate commercial and housing sectors as well as infrastructure development.

Latest financials and outlook

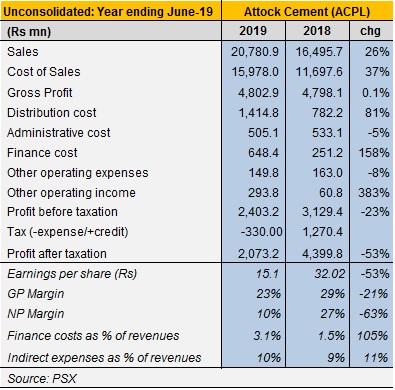

Clinker exports have grown by 15 times in 9MFY19 against last year. During this period, exports were 45 percent of total sales, which was improved on the back of the new production line becoming operational as domestic demand waned. In FY19, Attock's revenues grew by 26 percent according to the PSX notice. However, margins came down to 23 percent owning to higher costs of production. Coal prices averaged a few dollars higher than the previous year while the rupee has depreciated by over 30 percent since July-17.

Rising costs of borrowing, and higher distribution expenses owing to greater exports also grew the company's expenditure-increasing to 13 percent of revenues against 10.5 percent in FY18. Further monetary policy tightening will put pressures on the expense side of the P&L and squeeze profit margins. Meanwhile, coal prices and the expensive dollar will hurt gross margins.

It is also worth noting that clinker exports fetch lower prices than cement exports and domestic sales. Sales mix leaning toward clinker isn't the best for margins either.

As for domestic demand, austerity has slowed down private as well as public sector spending in development and infrastructure. This is not expected to change much as the new fiscal year kicks in. The company will likely be growing its reach to market overseas which is a good contingency plan if any.

Comments

Comments are closed.