Being among the pioneering and leading insurance companies, EFU General Insurance Limited (PSX: EFUG) has come out well amid increased competition in the general insurance segment. The firm was incorporated in 1932 and is part of the largest insurer group in the country - EFU, which also consists of EFU Life Assurance Limited and Allianz EFU Health Insurance Limited.

EFUG has increased its product portfolio over the years and the company provides a full range of insurance services to both the commercial and individual clients. EFU General's product portfolio includes Fire and Property Damage, Marine, Aviation and Transport, Motor and others, besides Window Takaful operations that initiated in 2015 and other value added services. EFU General also has a separate Risk Management Team and Engineering Group that work closely with clients to identify various risk exposures.

The non-life insurance company has also EFU General also has a separate Risk Management Team and an Engineering Group who work closely with clients to identify various risk exposures. It is rated Insurer Financial Strength AA+ by the rating agencies with a stable outlook.

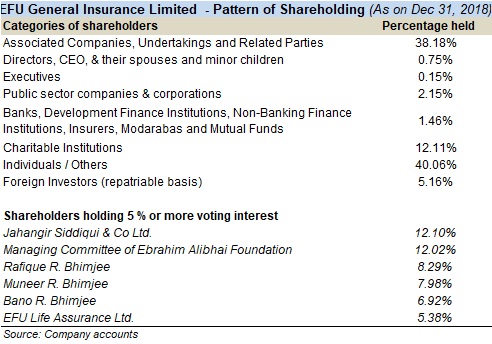

The shares of EFU General are quoted on Pakistan Stock Exchange. Over the last one year, it can be seen that the insurance company has largely beaten the benchmark index. The company's shareholding pattern is such that 20.6 percent of the firm is held by Jehnagir Siddiqui and Co., while around 12.6 percent is held by charitable organisations and institutes. Directors, CEOs, their spouses and minors hold 17.69 percent. A breakup of the shareholding is given in the illustration.

Insurance sector overview

Insurance sector penetration to GDP remains very low in Pakistan, only between 0.7-0.9 percent. This is largely due to lack of awareness as well as due to the existence of a large undocumented economy. As per the latest available information in SBP's Financial Stability Review released last year, the sector overall saw a growth of around 10 and 12 percent in gross written premium - revenues for the insurance companies - in CY16 and CY17 respectively.

Key factors for growth in the asset base and the premiums in CY17 for the industry were growing economic activity, ease of structural constraints such as allowing conventional insurers to transact window Takaful business and issuing relevant regulations to achieve uniformity, relatively low inflation and use of technology based distribution channels.

Profitability of the sector in the last couple of years however has seen a dip primarily due to low interest rate environment and hence lower investment income - a key component to lift earnings for insurance companies. A key rising trend in the non-life insurance segment in the country has been the growth of Islamic insurance - known as Takaful. Significant growth was reported by the Takaful segment due to the influx of conventional insurers in the Takaful market in the form of Window Takaful Operators (WTOs).

In non-life insurance companies, it has been seen that the gross and net premiums have grown over the last few years. However, the decline in investment income and a rise in underwriting expenses have pushed the profitability of the sector down. Motor segment continues to be the largest sector of the portfolio in terms of net premiums. Where net premiums have grown, net claims have also shown similar large increase

Financial and operational performance

EFUG has seen growth in premiums (net) over the last five years. Year-on-year premium growth peaked in 2017 - 19 percent - and then dropped to only 2 percent in 2018. The firm's past performance has also seen improvement in its claim ratio (or loss ratio) in the last five years. The loss ratio indicates the company's loss experience as a proportion of premium income earned during the year. On the other hand, EFUG's earnings have remained stable over the last three years.

For non-life insurance companies, investment income has a lot of significance in the firm's profitability. It usually makes up a larger proportion of the total income, acting as a buffer whenever the technical income falls short. This can be seen in the illustration; EFU General's incomes from investments were around 78 percent in 2015, because the insurance company witnessed a significant fall in underwriting profits. Over the next three years the increase in underwriting profits' share can also be seen.

Risk retention ratio, which indicates the level of risks retained by the insurer, can be seen to fall for EFUG. Retaining less risk means spreading the risk, where reinsurance plays an essential role.

In 2018, EFUG's net premium earned continued to grow. However, the underwriting profits slipped as expenses were higher. Expense ratio which reflects the efficiency of insurance operations and shows a significant jump in 2018 after falling for three consecutive years.

Outlook

Being one of the biggest players in the private non-life insurance segment, EFUG enjoys a significant market share of around 24 percent for 2018. And because of its position in the sector, the company is poised for growth as it continues to introduce new products as well as strategize old ones.

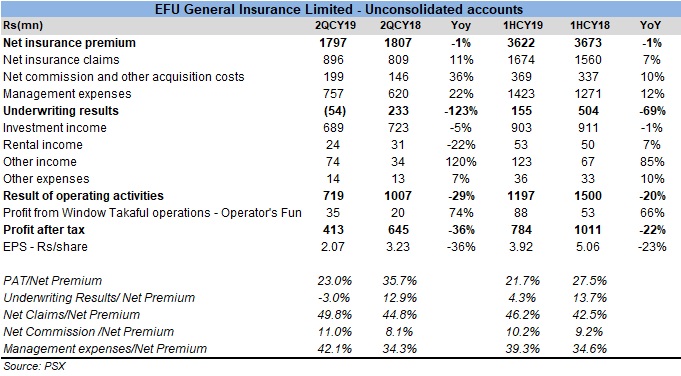

With economic activity taking a dip in 2018 and 2019, prospects for the non-life insurance sector have been tainted by higher inflation and lower industrial activity. During the 1HCY19, EFUG saw its earnings come down by 36 percent year-on-year. Its net insurance premiums showed no growth in 1HCY19 and 2QCY19, which is one factor in squeezing the bottom-line. Its underwriting results turned sour during the 2QCY19 and dropped by almost 70 percent in 1HCY19 due to cost increase be it net claims, commissions or management expenses. Hence, the underwriting results to net premium ratio fell from 12.9 percent in 2QCY18 to negative 3 percent in 2QCY19.

Growth in investment income remained flat in 1HCY19. However, it dropped by around 5 percent due to the turbulence in the stock market in the latest quarter. The investment income largely constitutes dividend income as well as income from equity and debt securities. Nonetheless, with a share of 25 percent in 1HCY19 total revenue (net premium) for EFUG, investment income played its role in lifting the company's earnings.

Despite increasing premium revenues and the rising interest rate environment that can aid the company and the sector in raising more investment income, it seems that the opportunity based on growing economy is slipping away. However, CPEC development of SEZs and prospects of Takaful can help the general insurance companies turn tides over.

Comments

Comments are closed.