Gadoon textile Mills Limited (PSX: GADT) was incorporated in 1988 by Yunus Brothers Group (YBG) as a yarn producing spinning mill. YBG is a conglomerate with domestic presence, formed in 1962 as a trading house, which over the course of four decades ventured into textile, cement, construction and power generation sectors with an annual turnover that exceeds $750 million. More popularly, the group owns Lucky cement, which happens to be the biggest cement manufacturer in the country.

GADT originated in the Amazai area of district Swabi, KPK, and later expanded operations to Karachi, Faisalabad and Lahore. It is primarily involved in manufacturing different kinds of yarn and knitting fabrics with B2B arrangements in place. Majority of the revenue stems from domestic operations while exports have averaged at 35 percent in the past five years. The production facility is capable of processing all categories of cotton and manmade fiber. Manufacturing involves processing raw cotton fibre into yarn with means of spindles. The company is currently equipped with a modern environmental friendly plant which utilises waste recovery.

Early operations began with a little over 14,000 spindles, which as of now has grown into more than 300,000 spindles. The overall industry has a capacity of 11.3 million spindles. Spinning sector comprises of about 315 spinning mills as represented by All Pakistan Textile Manufacturers Association (APTMA), out of which 85 are listed on the stock exchange as of 2019.

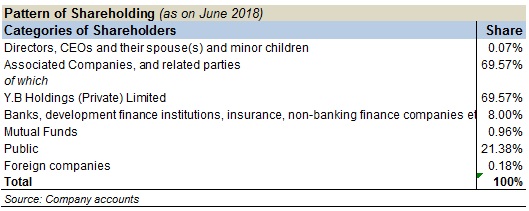

Shareholding pattern

GADT's shareholding pattern is highly concentrated with the Yunus Brother Group holding almost 70 percent of the total outstanding shares as at Jun-18. This is followed by the general public, which holds 21 percent while banks, DFIs and insurance companies cumulatively have 8 percent ownership of Gadoon Textile Mills Limited.

Industry dynamics

The textile industry comprises of an interlinked value chain. The process begins with cotton ginning that requires extracting cotton fibre from the seed, which is then converted to yarn through the spinning process. Yarn is then knitted into fabric, which then goes through the final stage of dyeing before being retailed. Ginning, spinning and knitting are sub sectors within the textile industry and a composite in a vertically integrated company that operates across the entire value chain. As mentioned above, Gadoon operates in the spinning and knitting segments.

Cotton being the primary raw material in the textile value chain is of utmost importance. In FY19, domestic cotton production stood at 10.77 million bales against national requirement of about 13-14 million bales annually-the shortfall is imported. The gap is mainly attributed to low returns to growers, higher cost of production, low yield and attack of viruses and pests.

Being a major contributor to the GDP and a primary contributor to exports (60% of all), the textile sector has gone through long periods of tax incentives and subsidised financing facilities but has also faced issues such as higher energy pricing and refunds stuck with the government for months at end causing massive liquidity crunch, especially amongst textile SMEs. Refund claims under Drawback of Local Taxes and Levies (DLTL) scheme, for instance are still stuck with the government.

The PTI came into power proposing a textile policy that aimed to tackle the high cost of doing business within the textile industry while promoting and incentivising value addition within the industry among other key areas. This fell in line with the Textile Policy 2014-19. The PTI proposed that electricity prices will be revised downward to USc7.5/KWh and a uniform gas rate across the country at rate of $6.5/mmbtu. The latter was proposed in the mini-budget in Sep-18 worth Rs44 billion. Under the Finance Bill (amendment) 2018, there was also a cut in regulatory duty on the import of raw material by the textile and other exporting sectors.

While Gadoon's annual report for FY18 claims that the company enjoyed growth in exports that year due to the government export package, the APTMA argues that the Textile Policy failed to achieve any of its lofty targets such as doubling of exports, doubling of value-addition, and so on. Because of the financial crunch, many of the schemes could not be implemented. Sources within the Business Recorder claim that of the Rs64 billion planned financing, only Rs 10 billion was spent on the implementation of different schemes. The energy subsidies were later on retracted. Clearly the government is not in the position to dole out subsidies. Since then, the incumbent government has also made changes to the tax regime on sales and increased withholding taxes on the value chain, up from 1 percent to 4 percent.

Recent financial performance

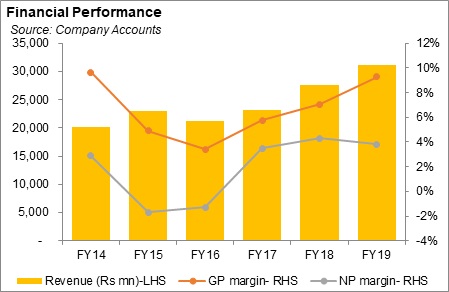

Despite a slowdown in the economy during FY19-and other sectors suffering at the hands of it-Gadoon's financial performance has remained strong. Revenue increased by 13 percent during FY19 brought forth mainly by domestic sales. This is in fact in line with the CAGR for the past three years recorded at 14 percent. Cotton yarn is the major segment for GADT, which comprises of more than 90 percent of the total revenues. Fabric takes up the rest. During FY19, about 72 percent of the revenue came in through domestic sales. Exports in the past five years have averaged about 35 percent of the total revenue stream.

However, exports declined 13 percent year on year despite dollar strengthening by 34 percent in value year on year, and its share in total revenue dropped to 27 percent versus 37 percent. This is attributed to fewer textile orders as the world is engulfed in a US-China trade war. Price per unit for cotton yarn exports also remained largely flat. Meanwhile, the export rebate Gadoon enjoyed during FY18-mentioned above-was also not available.

The company channeled its cotton yarn towards domestic markets-particularly targeting value-added yarn-as reflected by a 35 percent increase in domestic yarn sales during the fiscal year. Evidently, local demand remained strong. Cotton yarn prices also rose by an average of 23 percent during FY19 compared to the corresponding period which buttressed Gadoon's revenues.

In a high cost scenario, the company has managed to keep an upward trajectory for its gross margins. They improved from 7 percent in FY18 to 9 percent in FY19 supported by volumetric growth, higher cotton yarn prices and well-management procurement and inventories. The devaluation of rupee would have increased imported raw materials costs, while the company has also lately been shifting to imported raw material over domestic, but it has fared well on prices.

Raw material is a major component of costs (over 70%) while about 13 percent of costs goes into energy. In 2018, Gadoon's annual report argued that it altered the power consumption mix "by greater use of natural gas against furnace oil, due to rising trend of furnace [that] year. Furthermore, the company is consistently procuring new and more energy efficient gas generators to avail maximum possible benefit by utilizing gas".

Decreased exports allowed the company to bring down its distribution costs. Overall, distribution and administrative costs together stayed at 2 percent of revenues in FY19 as last year. Meanwhile, higher finance costs-rising to 4 percent of total revenue from 2 percent-were on account of the company's recent BMR strategies financed through debt, where it is replacing old machineries with new technological advanced machineries. The CAPEX has added to the finance costs, which were further exacerbated by a cumulative 500 bps interest rate hike during the fiscal year.

Future outlook

The company believes its capital expenditure into improving efficiencies will increase its market share and reduce external support for working capital requirement. If that actually happens, Gadoon may rely less on bank financing, which has become significantly more expensive lately. Rate hike may prove to be detrimental to the bottom line as it did during FY19.The Company has managed the currency depreciation pretty well so far. If demand abroad recovers, it may further incur benefit from the devalued rupee.

However, that also largely depends on the prices that it fetches in the international market as well as its raw material mix. If it imports more, any benefit from the devalued rupee may be diluted. Domestic sales may suffer as well. Friction in operations lie ahead as the incumbent government in an attempt to expand its tax net introduced a CNIC requirement throughout the value chain, which has resulted in unregistered companies to step back from conducting business as they do not want to be included in the tax net. GADT will be adversely impacted by this policy as the company depends mostly on domestic sales and supplies to many of these domestic businesses. The industry awaits a new textile policy, but it may be hard pressed to find one being implemented any time soon as the economy swims its way out of its current fiscal crisis.

Comments

Comments are closed.